At a glance

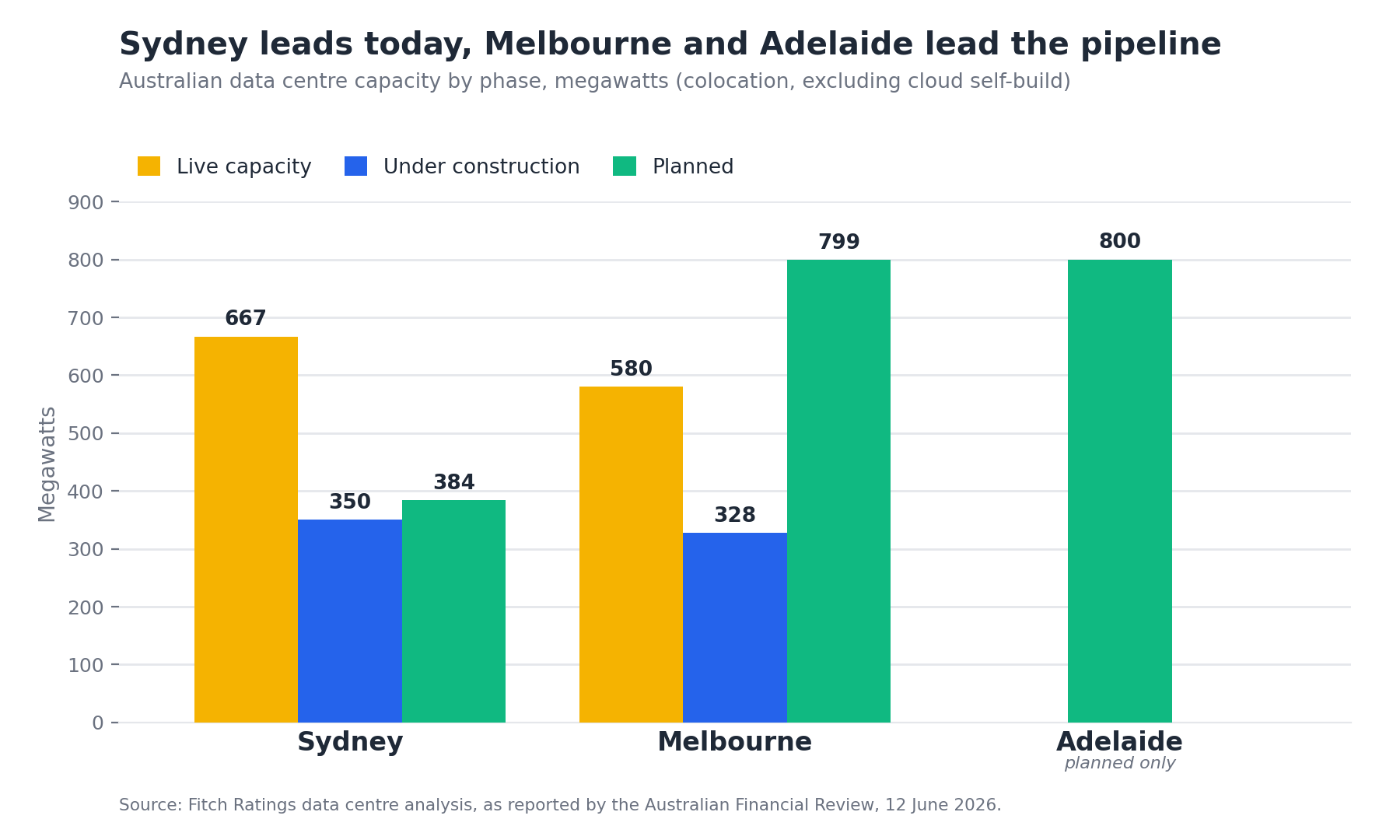

Melbourne now leads Sydney on planned capacity, 799MW to 384MW, even though Sydney still has more live capacity (667MW to 580MW) and more than 90 operating data centres to Melbourne’s 55.

Data centres drove the March quarter’s record 16.3 per cent rise in machinery and equipment, the biggest in 30 years, but most of the kit was imported, so the net lift to GDP was modest and Australia booked its first trade deficit in a decade.

In the United States, data centres were about 4 per cent of the economy in the first half of 2025 but roughly 92 per cent of its growth.

One proposed Sydney facility at Lane Cove West drew 374 objections and nine submissions in favour.

Adelaide has 800MW in planning, IREN is building 800MW in South Australia, and operators are moving into Perth and Darwin. The pipeline is national.

The lessons each state is generating on land, grid, water and community consent cross borders intact. The opportunity grows when the states share them.

Melbourne’s lead is in the pipeline

On the numbers everyone is quoting, Melbourne has edged in front. Ratings agency Fitch gives the city larger, more accessible land and fewer grid constraints, plus the pull of new cables in TalayLink, SMAP and Google’s Australia Connect. Amazon Web Services made the point concrete last year: it withdrew a Sydney application and pressed ahead in Melbourne.

The lead sits in the forward book, not the present. Sydney still runs more live megawatts and more operating sites. Melbourne wins once planning is counted, 799MW to 384MW, and Adelaide appears from almost nothing with 800MW in the queue.

What that chart really shows is a national market broadening out. Sydney’s prime land and grid capacity are increasingly spoken for, so the next wave of demand spreads to wherever it can be built and energised.

Growing barriers to entry in top-tier locations, particularly in relation to power availability, is spurring new developments across secondary markets where power, water and land availability are less restricted.

That is not a verdict on which city is winning but a read on where the boom goes next: out of the two majors and into Adelaide, Perth, Darwin and Tasmania. The industry already counts the build as one number. The first Data Centres Australia and DC Byte forecast, set out in our five themes from a remarkable quarter, puts operational capacity at 1.4GW today and 3.2GW by 2030, inside a 21.6GW national pipeline. None of it stops at a state line. The Fitch table and that 21.6GW figure measure different stages: Fitch counts nearer-term, named projects, while DC Byte’s headline includes 16.8GW still early and uncommitted.

92 per cent of US growth came from data centres

Here is the number that should reframe the whole debate. Assistant Minister Andrew Charlton gave it to the Sydney Institute on 10 June. In the first half of 2025, data centres and the gear inside them were about 4 per cent of the United States economy and roughly 92 per cent of its growth.

Strip out that single category, and American growth in that period rounds to zero.

The prize here is just as big, and Australia can reach it, but it has to capture more of the chain to get there. The US hosts the chip designers, hyperscalers and AI labs, so its build feeds its own economy; Australia, for now, mostly imports the hardware. National output grew just 0.3 per cent in the March quarter even as business investment rose 6.0 per cent, driven by a record 16.3 per cent surge in machinery and equipment that the national accounts put down to data centre expansion in New South Wales and Victoria. The reason is the import bill: the spend that lifts the investment line also lands in the imports line, the two largely cancel, and the server racks helped produce Australia’s first quarterly trade deficit in a decade. The lasting gain does not come from the imported boxes but from what Australia builds and runs around them: the construction, the grid and renewable build, the operations, and the sovereign compute it hosts. We set out the same import dynamic in our ABS capex analysis.

Over time, the AI boom may have a more profound impact on the Australian economy than the resources boom.

374 objections, nine in favour

The risks travel as well as the money. The same week Charlton delivered his speech, he pointed to a single proposed facility at Lane Cove West that drew 374 objections and nine submissions in support. Residents raised noise, diesel backup generators and a building rising barely 160 metres from a primary school. In the United States, a Gallup poll last month found 71 per cent of people opposed data centres in their community.

This is not a Sydney problem. Every jurisdiction chasing capacity will meet the same questions, and the siting and community work that earns consent in one suburb is reusable in the next. Treating consent as shared learning is faster and cheaper than each state arguing it out alone.

One national standard?

Each government is writing its answer, and most of it transfers. Victoria’s Sustainable Data Centre Action Plan covers land, grid, water, coordination and workforce, and the state puts the prize at up to A$25 billion in capital. New South Wales recorded A$2.6 billion of data centre investment in 2024-25, growing 65 per cent a year over three years, in its March consultation paper, which we examined in detail. Over the top sits the federal triple lock: bring new power, pay your full grid connection, and run as a flexible load.

The competition between the states is real, but the trap is letting the scoreboard become the story. Our analysis of how NSW is competing for data centre capital reached the same conclusion: the contest has accelerated national capacity, and Data Centres Australia has welcomed the federal framework that holds every jurisdiction to one standard.

Power, fibre and talent ignore state borders

The constraints that decide this boom are national by design. AEMO’s queue holds 5.4GW of large-load data centre projects, roughly 60 per cent in New South Wales and 40 per cent in Victoria, on one National Electricity Market. Charlton put data centre use at about 2 per cent of the NEM today, with demand nearly doubling in Victoria and rising 18 per cent in New South Wales in a single year. Grid headroom in one state is not walled off from load in another.

Connectivity is built to cross borders too. SMAP links Sydney, Melbourne, Adelaide and Perth, and Firmus has agreed to build a new cable to Tasmania that feeds into it. A cable landing in one state carries traffic for all of them. The same goes for skilled people and capital, which pool nationally. A win in Adelaide or Perth strengthens a national pitch that already ranks Sydney second and Melbourne fourth among Asia Pacific’s primary markets on Cushman & Wakefield’s 2026 comparison.

The real prize is national

So Melbourne is ahead of Sydney this quarter but it is the wrong scoreboard. The money is national, the risks are national, the constraints are national, and the lessons each state is writing belong to the whole country. The capital has already chosen Australia. The task is to capture the full pipeline and set the terms once, well.

As Charlton told the Sydney Institute:

Whether Australians end up tenants in someone else’s digital future, or owners of our own.

The real test is whether Australia acts as one market. July is the moment to watch, when Commonwealth, state and territory energy ministers weigh the triple lock together. Around it the state pipelines convert, from the NSW Investment Delivery Authority’s first major round to Victoria’s A$25 billion plan and the new capacity rising in South Australia, Tasmania and the west. Power decides where it all lands, and most of the country already shares one grid and one set of rules.