At a glance

The ABS headlined yesterday’s March quarter capex release “Data centre investment drives new capital expenditure”, attributing the quarter’s lift to server racks and processing equipment.

Private new capex rose 6.5 per cent in the March quarter 2026 and is 14.6 per cent above the prior March quarter.

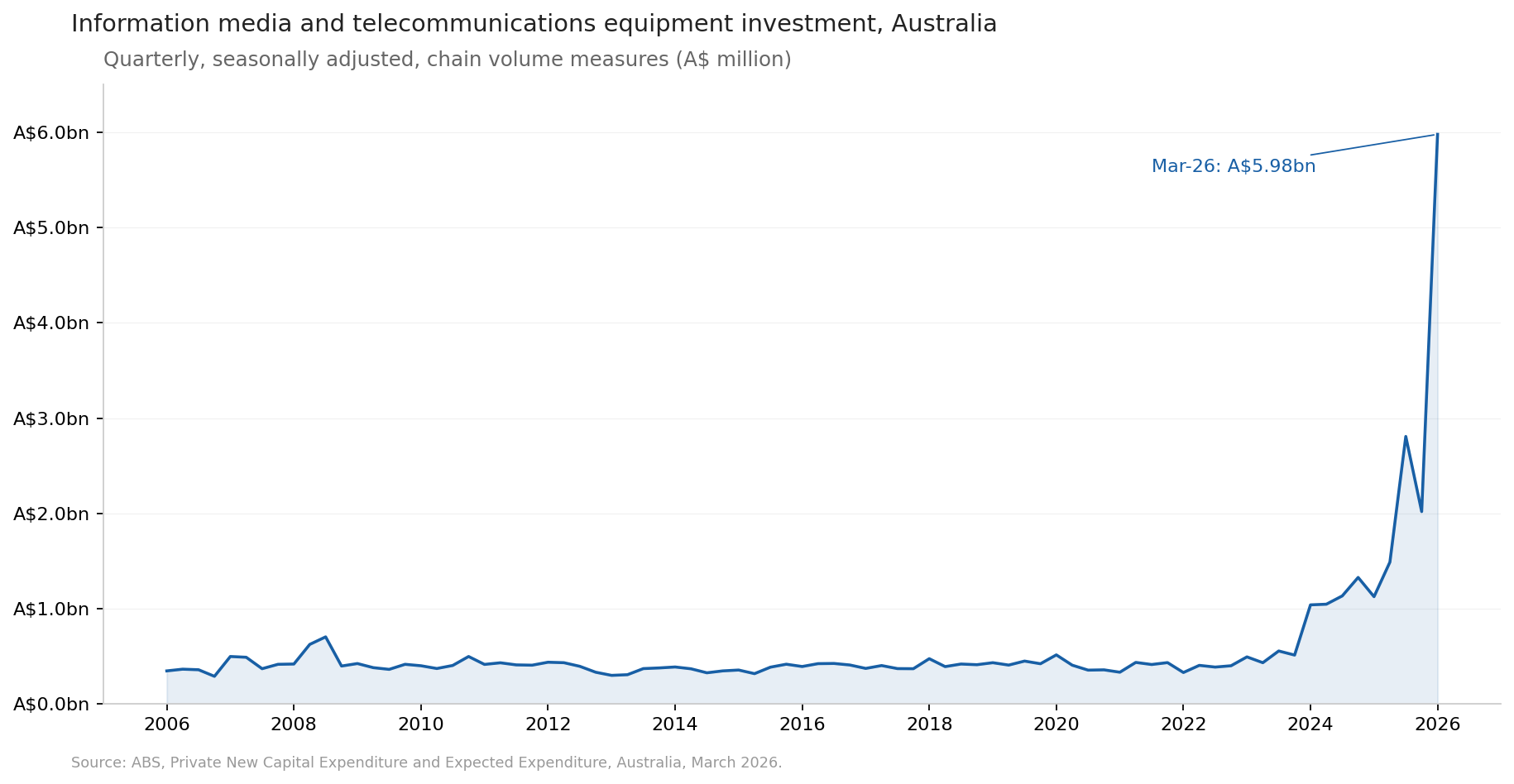

Information media and telecommunications equipment investment rose 196.1 per cent in the quarter to a seasonally adjusted A$5.98 billion, the highest on record.

Information media and telecommunications building investment rose 12.6 per cent, the seventh straight quarter of building gains in the segment.

NSW capex rose 22.1 per cent and Victoria 12.7 per cent. Every other state and territory recorded a fall except South Australia (+0.2 per cent).

Businesses revised expected 2026-27 capex up 9.9 per cent on the prior estimate, with the ABS attributing the upward revision to continued data centre investment.

The Australian Bureau of Statistics released the Private New Capital Expenditure and Expected Expenditure, Australia, March 2026 yesterday. The media release that accompanies it is titled Data centre investment drives new capital expenditure.

Tom Lay, the ABS head of business statistics, attributed the quarterly lift directly. “The lift in investment was the result of investment in data centre equipment, specifically server racks and processing equipment, significantly boosting overall investment figures,” he said. “This quarter’s rise builds on a similar spike in data centre investment recorded in the September quarter 2025.”

The ABS publishes quarterly capex releases on a fixed calendar. Naming a single industry segment in the headline of one is unusual. The Q1 2026 release elevates data centres to a macro economic line item in the agency’s framing. The release also references the Spotlight - Data Centres in Economic Statistics article published with last quarter’s release, which mapped where data centre activity now appears across the ABS suite of statistics.

What the numbers actually say

Private new capex rose 6.5 per cent in the March quarter, seasonally adjusted in chain volume terms, and is 14.6 per cent higher than the March quarter last year. Non-mining business investment rose 8.8 per cent. Mining was relatively unchanged.

Information media and telecommunications, the industry classification that captures data centre operators, recorded the largest industry rise, up 96.1 per cent to a new record level. Inside that industry, the equipment line is where the AI infrastructure investment shows up. Equipment investment for information media and telecommunications rose 196.1 per cent in the quarter to a seasonally adjusted A$5.98 billion. That is the highest reading in the history of the series.

For context, the same equipment line was A$1.13 billion in the March quarter 2025 and A$2.81 billion in the September quarter 2025. The March 2026 figure is more than five times the March 2025 figure and more than double the September 2025 figure. The 196.1 per cent quarterly rise is the change from December 2025 to March 2026 alone.

Quarter | Info media & telco equipment, seasonally adjusted (A$m) |

Mar-25 | 1,126 |

Jun-25 | 1,489 |

Sep-25 | 2,808 |

Dec-25 | 2,019 |

Mar-26 | 5,979 |

Source: ABS, Private New Capital Expenditure and Expected Expenditure, Australia, March 2026.

New equipment and machinery investment across the whole economy rose 18.1 per cent in the quarter, also the highest in the history of the series. Non-mining equipment and machinery rose 20.1 per cent. Mining equipment and machinery rose 7.2 per cent. The data centre line accounts for the bulk of the non-mining figure.

Most of the equipment behind the ABS capex line is imported. NVIDIA supplies the GPUs at the centre of every Australian AI deployment publicly disclosed so far. Dell, HPE, Supermicro and Lenovo build the rack-mounted server systems those GPUs go into. The racks and surrounding power infrastructure come mostly from Schneider Electric, Vertiv, Eaton and Rittal, which together hold roughly half the global rack market. The Australian deals fit the same pattern: Macquarie Data Centres has paired Dell PowerEdge XE9680 systems with NVIDIA chips at IC3 Super West in Sydney; Sharon AI is deploying NVIDIA B200 GPUs at NEXTDC M3; Firmus runs 26,000 NVIDIA chips at its Tasmanian facility. On the Australian-listed side, Dicker Data is the largest distribution conduit and reported 13.4 per cent FY26 revenue growth partly on data centre demand.

The building vs equipment split

Buildings and structures investment fell 3.8 per cent in the quarter across the economy. Lay attributed this to “large projects reaching completion, particularly across manufacturing, electricity, gas, water and waste services and mining.”

But the data centre cohort moved the other way on buildings. Lay continued: “Despite the overall fall, investment in data centre building construction continues to grow with information media and telecommunications rising for the seventh straight quarter, up 12.6 per cent.” Information media and telecommunications building investment is now A$2.72 billion, up from A$1.87 billion a year ago.

The shape of the cycle this reveals is consistent with what Certified Strategic has tracked across the operator pipeline. Land has been acquired. Shells are still going up. Equipment is now arriving at scale. Buildings continue to rise at a steady 5 to 15 per cent quarterly clip across seven quarters. Equipment has accelerated 5x year-on-year in a single line item.

NSW and Victoria are absorbing the build

The state breakdown maps directly to the operator pipeline. NSW capex rose 22.1 per cent in the quarter. Victoria rose 12.7 per cent. South Australia rose 0.2 per cent. Every other state and territory recorded a fall.

NSW and Victoria are the two states where the bulk of the hyperscale and AI factory pipeline. AirTrunk’s 1.2 GW Mamre Road campus, NEXTDC’s S7 Eastern Creek site for OpenAI, NEXTDC’s M4 campus at Fishermans Bend in Port Melbourne, and Firmus’s Melbourne stages of Project Southgate are all NSW or Victoria assets. CDC’s 555MW US customer deal announced 6 May 2026 will also be delivered across its east coast campus pipeline.

South Australia’s marginal 0.2 per cent rise is the only third-state positive in the quarter.

The forward guidance is the leading indicator

Past-quarter actuals are historical. The forward expected capex revisions are where the operator commitments show up.

This release contains the sixth estimate for 2025-26 and the second estimate for 2026-27. Businesses revised 2025-26 expected capex up 4.5 per cent on the previous estimate. They revised 2026-27 expected capex up 9.9 per cent on the first estimate published in the December 2025 release. Lay attributed both upward revisions to continued data centre investment.

The 9.9 per cent 2026-27 revision is the forward-looking signal in this release. It says the operators surveyed by the ABS now expect to spend materially more in financial year 2026-27 than they thought they would just three months ago. The reading is forward order book. It is happening inside two ABS revisions of an already-record-high baseline.

The operator pipeline is now visible in the national accounts. A$5.98 billion of server rack and processing equipment in a single quarter is consistent with the hyperscale GPU clusters being commissioned at NEXTDC, CDC, AirTrunk and Firmus Australian facilities.

The 9.9 per cent upward revision to 2026-27 expected capex says the operators surveyed expect to keep spending. The 12-to-18-month window we flagged earlier this year is now showing up in the forward capex estimates, not just in operator announcements.

What to watch

The June quarter release, due in late August 2026, will show whether the September 2025 to March 2026 acceleration was a step-change or a single spike. The Sep-25 to Mar-26 trend now has two record quarters separated by one softer reading (Dec-25 at A$2.02 billion equipment). The next print determines whether this is a structural lift or a lumpy delivery schedule.

The seventh-quarter rise in information media and telecommunications building investment will start to plateau as land-and-shell construction completes on existing campuses. When it does, the equipment line should keep rising as those shells fill with GPUs. A flattening building line alongside a still-rising equipment line is the next phase signal.

The 2026-27 expected capex revision in the June quarter release. A further upward revision would confirm forward commitment. A flat or downward revision would suggest the current quarter is the cyclical high.