At a glance

The South Australian government on 23 June 2026 released a data centre strategy to attract AI infrastructure investment, with government modelling putting a 1GW campus at about A$6.8 billion in capital expenditure, an estimated 500 to 1,000 construction jobs and 200 to 300 ongoing roles.

The centrepiece is a faster, coordinated planning path: data centres can be treated as essential infrastructure in exchange for bringing new firmed renewable supply, the principle the government calls “new energy for new demand”.

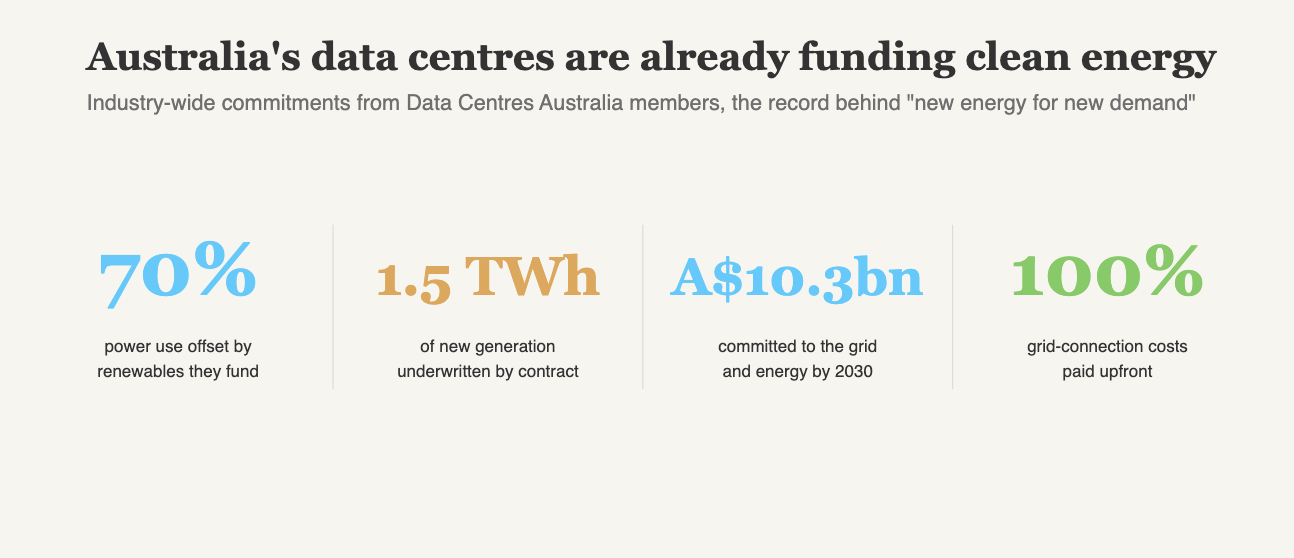

The approach builds on what the national industry already does. Data Centres Australia members fund 70% of their power use from renewables themselves, have underwritten 1.5 TWh of new generation, and have committed A$10.3 billion to grid and energy infrastructure by 2030.

IREN’s planned 800MW Bundey campus, reported at around A$10 billion, is the working model: a large anchor load that finances new clean energy in a renewable energy zone.

The Act would also set water-efficiency, grid-stability and fair-network-cost conditions. It has been announced, not yet introduced to state parliament.

AirTrunk welcomed the strategy the same day, highlighting jobs, skills development and long-term regional benefits.

South Australia opens the door to AI data centre investment

Premier Peter Malinauskas released the strategy on 23 June 2026, telling reporters the state needs data centres and intends to win its share of the AI build-out. As reported by the ABC, the government plans to introduce new laws into state parliament to give the sector its own pathway rather than leaving it to existing planning rules. The legislation has been announced, not tabled, so the operative detail will sit in a bill that does not yet exist in public form.

The pitch is built for an Australian audience watching capital chase clean power. South Australia runs the highest wind and solar share of any mainland grid and is targeting 100% net renewable electricity by 2027, which is exactly what a power-hungry AI campus wants. Government modelling cited with the strategy puts a 1GW data centre at about A$6.8 billion in capital expenditure, with an estimated 500 to 1,000 construction jobs and 200 to 300 ongoing roles, and the state has already drawn IREN’s planned 800MW campus at Bundey. The strategy is a move to convert that interest into committed projects.

What the Data Centre and AI Infrastructure Act would offer

The strategy frames the deal plainly: bring new power, and the path to building gets faster. The anchor condition is “new energy for new demand”, under which developers match demand growth with new, firmed renewable supply, so each new load is served by generation and firming the developer brings or contracts rather than by existing supply. In South Australia the binding constraint is firming. South Australia already has the clean generation; the value a large anchor customer adds is the firming, the batteries, transmission and dispatchable capacity that a long-term contract helps finance.

Three further conditions sit alongside it: fit-for-purpose water supply with efficient closed-loop cooling, which the strategy positions around the state’s proposed Northern Water project rather than stressed local river systems, support for grid stability with transparent reporting on energy use, and a fair share of network costs. Recycled-water cooling, as in AWS’s new Melbourne data centre, is one practical answer to the water question. The conditions track the economics behind the 2026-27 default-offer cuts: data centres are net positive for the system when they fund their own supply, pay their own connection costs, and add flexibility. South Australia is proposing to make that the standard for building, which is close to how the strongest operators already run.

The grid case for new firmed supply

The opportunity is sharpest where the grid is tightest. When regulated bills fell across most of the country on 1 July 2026, South Australia was the one state where the default offer rose, up 1.4%, on transmission constraints and continued gas dependence, a pattern we detailed in why Australian power bills are falling. Large, creditworthy loads that sign long-term contracts for new firmed renewable supply are one of the few forces that can finance the generation and storage the state needs, and the strategy is designed to channel exactly that.

The national industry already operates this way, and at scale. Data Centres Australia reports that members offset 70% of their power use with renewables they fund themselves, have underwritten 1.5 TWh of new generation through long-term contracts, and have committed A$10.3 billion to grid and energy infrastructure by 2030, paying their connection and augmentation costs upfront. South Australia's strategy would make that voluntary practice a condition of building.

Industry-wide commitments reported by Data Centres Australia.

800MW campus at Bundey

On 3 June 2026, IREN signed a transmission connection agreement for a planned 800MW campus at Bundey, roughly 125km northeast of Adelaide, securing four 330kV feeder exits sized to carry the full load without network upgrades and targeting first power from 2028. IREN cited South Australia’s target of 100% net renewable electricity by 2027, submarine fibre into Singapore, Indonesia, South Korea and Japan, and a state government acting on AI.

Bundey is, in effect, the working model the strategy promotes. The campus anchors to a renewable energy zone, takes a connection sized for its own load, and sits beside the storage and transmission that firm the grid. Reported at around A$10 billion, it shows what a single anchor customer can pull into a region: clean generation, transmission headroom and skilled jobs. The move also broadens a national pipeline that has clustered on the eastern seaboard, the dynamic we examined in the data centre boom as a national opportunity.

Operators welcome the strategy’s community focus

The first operator response came within the hour. AirTrunk, which is building past 630MW in Melbourne, said in a post on the strategy that what stood out was the emphasis on benefits beyond the data centre fence line: jobs, skills development, stronger energy infrastructure and long-term regional growth. The company framed those outcomes under its community-investment approach and said the real opportunity lies in how the investment creates lasting value for local communities. AirTrunk’s response, focused on jobs and community benefit, reads as the sector treating the strategy as an invitation rather than a barrier.

A faster planning path for projects that bring their own power

In exchange for bringing firmed supply and meeting the water and grid conditions, developers gain a faster route to approval. The strategy coordinates assessment across government, designates data centres as essential infrastructure, and builds on September 2025 amendments to the Planning, Development and Infrastructure Act that already let qualifying data centres be approved as state-significant development, with Office of the Technical Regulator and SA Water requirements kept in place.

The trade favours building. South Australia is offering certainty and speed to developers who arrive with their own power, turning the energy condition into a reason to choose the state. Concerns raised about water use and the pace of approvals, including by the Greens, are real, and the strategy’s water-efficiency and transparency requirements are the government’s answer to them.

How South Australia’s approach compares

South Australia is the first Australian jurisdiction to propose a dedicated Act that ties new firmed supply to a faster planning path. Other governments are moving on the same questions by different routes. The Australian Government issued national expectations for data centre and AI developers in March 2026, guidance used to prioritise projects rather than binding law. New South Wales, which hosts about 60% of the national connection pipeline, has consulted on five principles including a requirement that developers fund their own energy and water infrastructure, with a Legislative Council inquiry due to report by 30 September 2026.

Jurisdiction | Main instrument | Energy and supply condition | Planning approach |

South Australia | Proposed Data Centre and AI Infrastructure Act | New firmed renewable supply required (“new energy for new demand”) | Essential-infrastructure status, coordinated fast-track |

New South Wales | Consultation paper, five principles (under review) | Developers to fund their own energy and water infrastructure | State Significant Development, performance-based |

Australian Government | National expectations for developers (guidance) | Expected to underwrite new generation and grid | State-led planning |

Source: Published government documents, June 2026.

South Australia goes further than the others on one point: it would write the firmed-supply condition into legislation and pair it with a faster route to approval, using its renewable grid as the draw.

What to watch

Three items will shape how much the strategy delivers. The first is the bill itself: the timing of firming matters, because new supply works best for the grid when it lands with the load, and only the legislation will set that out. The second is the connection pipeline. AEMO’s Q1 2026 figures identified 11 large-scale data centre projects representing 5.4GW progressing through the transmission process, the demand the strategy is designed to capture, and we track the queue in our AEMO transmission pipeline analysis. The third is Bundey, and whether South Australia’s flagship moves from a signed connection toward construction as the first proof the model works.