At a Glance

~2,700+ data centre and AI infrastructure roles currently open across Australia

$100b+ in committed data centre and AI infrastructure investment this decade

0.7–1.7 GW projected capacity supply gap by 2028

300,000 construction worker shortfall by mid-2027 — five sectors fighting for the same talent

39% of high-value roles now require NV1 or NV2 security clearance

76% of new AI server deployments forecast to be liquid-cooled by end of 2026

6 new employer categories now active in Australian DC hiring that had no local presence two years ago

The Australia's data centre labour market has become one of the most consequential hiring markets in the country, sitting at the intersection of national security, energy policy, construction capacity, and AI sovereignty. A sweep of the full market in April 2026 reveals approximately 2,700 open data centre roles on Indeed Australia alone, with hundreds more listed across LinkedIn, company career pages, and specialist recruiters. The employers range from hyperscalers running multi-billion-dollar campus builds to AI labs that opened their first Australian offices within the last 90 days.

The Scale of Hiring Has No Precedent

AWS leads the market with an estimated 170+ open roles across Australia, driven primarily by its Melbourne sovereign cluster build-out and Sydney operations. Globally, AWS lists over 2,500 data centre positions — Australia now accounts for a meaningful share of that pipeline. Microsoft follows with approximately 85 Australian roles as it completes the operational phase of its A$5 billion cloud infrastructure expansion announced in October 2023, expanding from 20 to 29 data centre sites across Canberra, Melbourne, and Sydney.

Behind the hyperscalers, the Australian-listed operators are scaling headcount in parallel. NEXTDC carries approximately 18 open roles as it builds out its M4 Melbourne campus and prepares for the 550MW S7 sovereign AI campus at Eastern Creek. CDC Data Centres is hiring across its operations as it expands from 372MW operational capacity with a further 453MW under construction, and plans to grow by an additional 1,600MW. Equinix's Australian operations team continues recruiting across its four Melbourne and multiple Sydney facilities.

Hyperscalers Dominate — But the Employer Mix Is Changing

The most significant shift in April 2026 is the composition rather than the volume of the hiring.

AI labs have arrived as infrastructure employers. Anthropic signed its MoU with the Australian Government on March 31 and is building a Sydney team that includes a Transaction Principal — a compute infrastructure deals role, not a research position. The company is exploring data centre investments and energy partnerships aligned with the government's new expectations framework. OpenAI has two Sydney roles tied to its $7 billion NEXTDC partnership, including a National Security Lead covering Five Eyes government engagement.

Firmus, backed by Nvidia and Coatue at a USD $5.5 billion valuation, raised $505 million in its latest round and is targeting a $2 billion ASX IPO in mid-2026. Its hiring for proprietary HyperCube immersion cooling roles represents an entirely new skill category in the Australian market. CBRE is actively recruiting shift technicians, electricians, and apprentices for hyperscale data centre managed services in Melbourne's Derrimut corridor.

As we analysed in our Anthropic APAC hiring signal piece, the arrival of AI labs as physical infrastructure employers is not a temporary phenomenon, it is a permanent expansion of the employer landscape.

The Sovereign Shift Is Now a Hiring Pattern

Across the high-value end of the market, security clearance has become a gating requirement. CertifiedStrategic's analysis of strategically significant roles found that approximately 39% require or reference NV1, NV2, the SOCI Act, or PSPF frameworks.

AWS's Melbourne cluster positions all require NV1 clearance. Google's Technical Program Manager for Data Center Compliance requires NV2. Microsoft's Melbourne roles demand Australian citizenship and NV1/NV2. OpenAI's National Security Lead covers sovereign AI policy across Five Eyes nations.

The Australian Government's March 2026 expectations framework has accelerated this dynamic. Operators seeking streamlined regulatory support must demonstrate alignment with national interest criteria — and that means sovereign-cleared workforces. The AEMC's draft grid connection rule changes published in March 2026 add further regulatory complexity that will require specialist compliance capability.

For candidates: NV1 takes approximately three months to process, NV2 takes five. If you don't have clearance and you want access to the highest-paying tier of the market, the time to start is now.

Browse current data centre and AI jobs

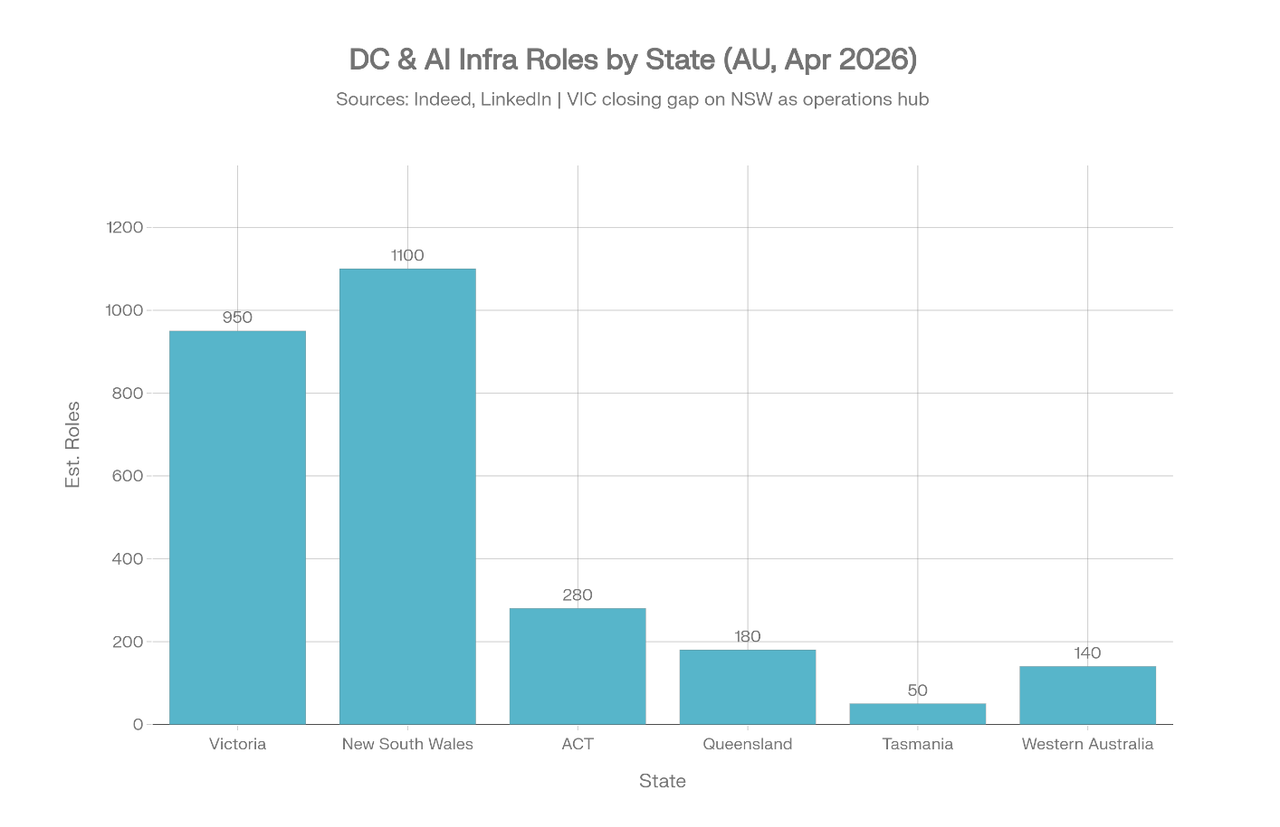

Victoria Is Closing the Gap on New South Wales

NSW retains the largest total share of data centre roles, anchored by Sydney's position as Australia's interconnection hub and the concentration of hyperscaler headquarters. But Victoria is closing fast. An estimated 950+ roles are now open in Victoria, driven by AWS's Melbourne cluster build-out (34+ roles alone), the operational phase of Microsoft's sovereign cloud campus, NEXTDC's $2 billion M4 AI campus at Fishermans Bend, CDC's Brooklyn expansion, and CBRE's Derrimut managed services operation.

Melbourne's structural advantages are compounding: cooler climate delivering better PUE performance against the government's 1.3 target, available industrial land in western corridors, and a growing base of operational talent. Victoria is becoming Australia's data centre operations centre while Sydney remains the interconnection and construction headquarters.

The ACT holds a notable 280+ roles, driven almost entirely by sovereign cloud requirements for Canberra-based government agencies. Queensland and Western Australia are emerging but remain early-stage — Schneider Electric's Brisbane hire for a data centre pre-sales role is one of the first of its kind in the state.

The Grid Bottleneck

CBRE forecasts a supply gap of 0.7–1.7GW by 2028. Australia's deployable capacity sits at approximately 1.35GW today. Even with aggressive building, projected live capacity of 1.8GW by 2028 will fall well short of demand estimates of 2.5–3.5GW.

The constraint is not land or compute hardware — it is grid connection. Operators can build a facility in 18–24 months, but grid connection and transmission upgrades take five to ten years. AEMO projects data centres will consume approximately 6% of NEM grid-supplied electricity by 2030, up from around 2% today. The government's March 2026 framework now requires operators to underwrite new renewable power supply and fund new grid connectivity.

This is creating entirely new role categories. Eaton's Grid Connection Engineer in Mascot exists specifically to navigate NSP and AEMO grid connections for 50MW+ facilities. Battery energy storage (BESS) integration, AEMO compliance, and renewable power purchase agreement management are all becoming standard requirements in data centre operations teams.

The $100 Billion Investment Pipeline

The hiring surge is underwritten by the largest wave of infrastructure capital Australia has ever absorbed in a single sector. Firmus's Project Southgate programme is valued at $73.3 billion (per Firmus investor disclosures), targeting 1.6GW of liquid-cooled AI compute nationally. AWS has committed AUD $20 billion to Australian infrastructure by 2029. OpenAI and NEXTDC's S7 campus represents $7 billion. Microsoft's cloud infrastructure programme is A$5 billion.

Mandala Partners' research, commissioned by five of Australia's largest data centre operators, forecasts new investment in Australian data centre capacity will top $26 billion by 2030. The CEFC estimates total hyperscaler commitment at $85–135 billion over the decade.

The Talent War: Five Sectors, One Workforce

According to Deloitte's March 2026 analysis of US and global markets, data centre job postings for core technical roles surged 64% between 2023 and 2025, while the broader economy grew just 4% for the same positions. More than one-third of new postings in both the data centre and power sectors target the same workers. 63% of data centre executives surveyed cited skilled labour shortage as their number one obstacle.

Australia faces the same dynamic, amplified by competing national priorities. Data centres are bidding against:

Renewable energy construction — transmission lines, solar, wind, and battery storage installations all need the same electricians, HV engineers, and project managers

Housing construction — Australia is short 83,000 tradespeople; the ETU has explicitly warned that data centres "must not siphon existing skills away from important national priorities like housing"

Defence and national security — the NV1/NV2 clearance pipeline is constrained and cannot be fast-tracked

Mining and resources — still the dominant employer of electrical and mechanical engineers in regional Australia

Infrastructure Australia projects the construction workforce shortfall will hit 300,000 by mid-2027, driven by a record $242 billion major project pipeline. The government's expectations framework explicitly requires data centre operators to invest in apprenticeships and workforce development.

The leverage is significant for experienced candidates. Those holding NV1/NV2 clearance with data centre operations experience, HV electrical qualifications, commissioning experience, or liquid cooling knowledge sit at the intersection of extreme demand and constrained supply. Goldman Sachs forecasts that 76% of new AI server deployments will be liquid-cooled by end of 2026, up from 15% in 2024, making immersion and direct-to-chip cooling expertise among the most valuable technical credentials in the sector.

What's Coming: Predictions for H2 2026 and Beyond

Firmus ASX IPO (mid-2026) will be the first pure-play AI infrastructure listing on the ASX. Expect a hiring surge around the listing as Project Southgate ramps nationally. A strong pricing validates a new asset class for Australian institutional investors.

Anthropic's Sydney team will expand into infrastructure partnerships. The Transaction Principal role is the leading indicator. Within two quarters, expect data centre partnership announcements and enterprise deployment roles.

AWS Melbourne will become the largest single-site hiring wave in Australian DC history. With 34+ roles already open and sovereign contract obligations accelerating, security-cleared candidates will be aggressively poached across sectors.

Grid connection engineering becomes a standalone discipline. As AEMC draft rules progress toward implementation, every operator seeking 50MW+ connections will need dedicated grid compliance capability.

Liquid cooling becomes non-negotiable for new builds. Goldman Sachs forecasts 76% of new AI server deployments will be liquid-cooled by end of 2026, up from 15% in 2024. The training pipeline for immersion and direct-to-chip technicians does not yet exist at scale.

The CBRE supply gap materialises as premium pricing for both capacity and talent. When the 0.7–1.7GW shortfall becomes visible in lease negotiations through late 2026, operators with grid-ready, certified sites will command pricing power.

Victoria formalises its position as Australia's DC operations hub. Watch for state government incentive packages specifically targeting data centre workforce development through H2 2026.

As we argued in our analysis of why Australia must win the race for sovereign AI infrastructure, the window to build is finite. The hiring patterns in April 2026 confirm the operators who understood this earliest are converting capital into headcount.

Browse current data centre and AI jobs

The Big Numbers

Metric | Figure | Source |

Open DC roles in Australia (Apr 2026) | ~2,700+ | Indeed Australia |

DC job posting growth (2023–25) | +64% | Deloitte (US/global) |

AU DC construction market (2025) | USD $7.3b | Grand View Research |

Projected market (2033) | USD $20.1b | Grand View Research |

Deployable capacity (2024) | 1,350 MW | AEMO / Industry |

Projected capacity (2030) | 3,100 MW | Government framework |

Supply gap by 2028 | 0.7–1.7 GW | CBRE |

Hyperscaler investment committed | $85–135b (decade) | CEFC |

AWS Australia commitment | AUD $20b by 2029 | Amazon |

Microsoft commitment | A$5b (announced Oct 2023) | Microsoft |

OpenAI / NEXTDC S7 campus | AUD $7b | NEXTDC |

Firmus Project Southgate | $73.3b (full programme) | Firmus |

Construction workforce shortfall (2027) | 300,000 workers | Infrastructure Australia |

DC share of NEM grid electricity (2030) | ~6% | AEMO |

Liquid-cooled new AI servers (end 2026) | 76% of deployments | Goldman Sachs |