At a glance

A single gigawatt of AI data centre capacity is now quoted at around A$50 billion to bring online in Australia, and at anywhere from US$50 billion to US$100 billion in larger offshore projects, depending on what the figure includes.

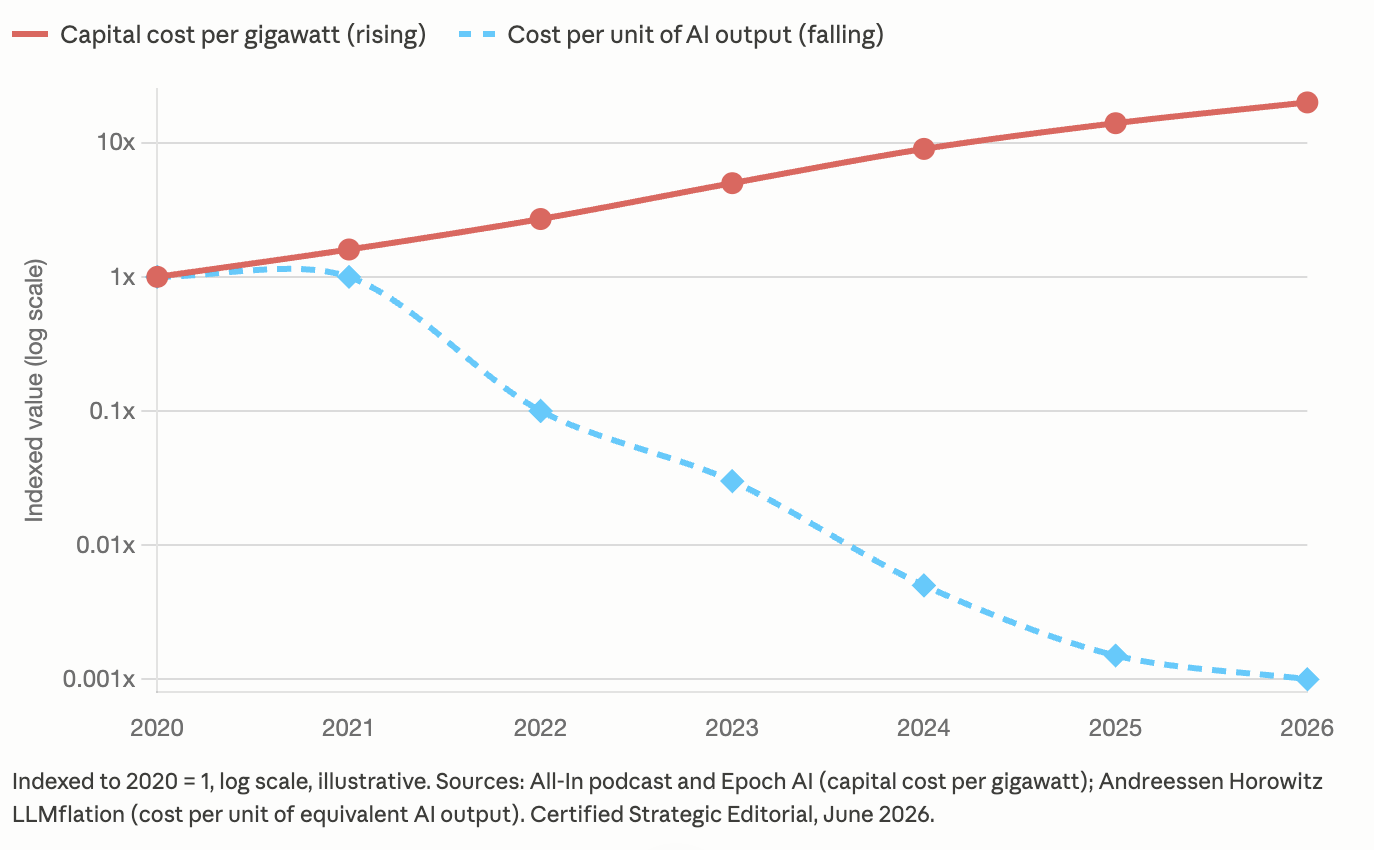

The capital cost of a gigawatt has risen sharply, but the cost of producing a given amount of AI output has fallen at roughly the same speed in the opposite direction.

By Andreessen Horowitz’s measure, the price of running a model of equivalent capability has dropped about tenfold a year for three years, close to a thousandfold in total.

NVIDIA frames the AI data centre as a factory that converts energy into intelligence, and states that the tokens produced within the same power budget have risen more than 1,000,000 times from its 2012 Kepler chip to the Vera Rubin platform this year.

AEMO forecasts data centre electricity use rising about 25 percent a year to around 12 TWh, close to 6 percent of grid-supplied power, by 2030, and now treats data centres as a distinct category in its planning.

For Australia, where power and the grid connection queue are the binding constraint rather than capital, output per watt may be a more useful yardstick to weigh alongside the build cost.

US$50bn to US$100bn a gigawatt

On the All-In podcast this month, alongside OpenAI’s chief financial officer Sarah Friar, investor Chamath Palihapitiya put the fully loaded cost of one gigawatt of data centre capacity at close to US$100 billion, against US$4 billion to US$5 billion when he first backed a project years ago. Friar put a gigawatt closer to US$50 billion on the same episode. Independent modelling by Epoch AI lands in between.

When the same gigawatt is costed anywhere from US$50 billion to US$100 billion, the gap is mostly about what each estimate counts. Land, power infrastructure, cooling and networking all sit inside it, and the compute hardware is the largest line item by a wide margin. Closer to home, an operator at the DCD Connect APAC investment forum in Bali put the cost of bringing a single gigawatt online in Australia at around A$50 billion, a marker of how far the economics have moved past traditional infrastructure. We covered that discussion in our report on the Bali investment panels.

On its own the number invites alarm; set against what a gigawatt now produces, it looks different.

20x the capital, a thousandfold cheaper output

Capital cost is an input, and it says little about output. A plant that costs twenty times more while producing fifty times more is the more productive of the two, and the way to see that is to measure what it produces per unit of power going in.

On that measure the direction is the opposite of the capital line. The price of running a model of a given capability has fallen about tenfold a year for three years, close to a thousandfold in total, on the LLMflation analysis published by Andreessen Horowitz. The comparison holds capability fixed: a task that needed a frontier model in 2021 now runs on a model that costs a fraction of a cent for the same result. Today’s frontier models do far more than the 2021 baseline, so the saving for a buyer who wants current capability is larger still.

That fall reflects rising efficiency rather than cheaper power, with each watt now producing more useful output. NVIDIA describes the AI data centre as a factory that turns energy into intelligence, and has made tokens per second per watt its defining efficiency measure. By the company’s account, the tokens generated within the same power budget have risen more than 1,000,000 times from its 2012 Kepler chip to the Vera Rubin platform this year, a figure set out in its performance-per-watt analysis. The number is the vendor’s own and reads as a direction of travel rather than an audited constant, but the trend it points to is visible across the market and shapes every facility design decision operators are making now, as we set out in our analysis of the GTC 2026 AI factory shift.

Charted together, the two move in opposite directions: capital per gigawatt rises while the cost per unit of output falls much further.

Power is Australia’s binding constraint

The reframe is useful everywhere, but in Australia it arguably matters a little more, because the scarce input here is grid power rather than capital.

AEMO has disclosed 5.4GW of data centre capacity moving through the transmission connection queue, with large connections targeting around a two-year path from application to energisation. In its Digital demand surge note of 1 June 2026, AEMO put data centres at about 2 percent of grid-supplied electricity today, rising to around 12 TWh and close to 6 percent by 2030, and now treats them as a distinct category in long-term planning. Power and the connection queue, not capital, decide which projects get built and when. Capital is mobile and is already arriving, a point underlined by the scale of the regional opportunity in the JLL Asia Pacific report and by the pace at which the neocloud tier has moved from concept to committed pipeline. AEMO also notes that large new loads can pull new supply forward, with data centres signing power purchase agreements that underwrite generation and storage.

When every watt is contested, the productivity of each watt is arguably worth weighing too. A megawatt connected in 2026 carries far more useful output than a megawatt connected three years ago, and the next generation of hardware widens that gap again. So one question worth adding for operators, investors and government is not only how many gigawatts Australia can connect, but how much output each connected watt produces once it is live.

Efficiency rises, demand still climbs to 2030

At CERAWeek 2026, NVIDIA and a group of energy companies, including Emerald AI, presented the AI factory as a flexible grid asset, one that can ease its draw when the grid is tight and reduce the need to build for peak demand. By their account, that flexibility turns large loads into a support for reliability rather than a strain on it.

AEMO’s published view sits a step back from that. Its analysis expects data centres here to operate, as things stand, as relatively inflexible loads that prioritise uptime and reliability, which is why it is tightening connection standards for large inverter-based loads through an AEMC rule change. Rising output per watt means each connected watt does far more useful work, but on AEMO’s current reading that does not change how those loads behave, and efficiency does not reduce the total power the system must supply, which AEMO still expects to climb steeply to 2030. Whether large loads can be encouraged to bend their demand and actively support the grid, as the NVIDIA and Emerald AI model envisages, is an open question. On the current evidence, efficiency looks like it changes what Australia gets for its energy more than how much energy the build-out will need.

What to watch

The capital-per-gigawatt figure will keep appearing in headlines, because it is large and easy to quote. Three angles seem worth putting beside it.

One is that capital does not look like Australia’s binding constraint. Grid connection does, and it is worth watching as the AEMO queue clears, as new connection rules take effect, and as the question of whether large loads can be encouraged to flex and support the grid moves from pitch to practice.

Another is that the efficiency curve seems to reward patience on hardware. Each GPU generation lifts output per watt, so the productivity of a connected gigawatt is not fixed at the point it is energised.

A third is that buyers who weigh output per watt, not just the sticker price, may judge projects and price contracts on a fuller picture than capital cost alone allows."