Highlights

Record colocation absorption of 963 MW in H2 2025, the highest half-year figure ever recorded in Asia Pacific

Vacancy down to 7%, with 78% of the 4.8 GW pipeline to 2027 already preleased

US$772 billion in capital investment needed across APAC to add 24 GW by 2030 (high growth scenario)

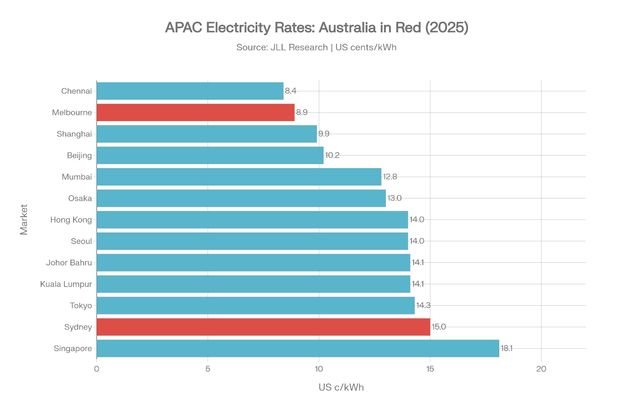

Sydney colocation electricity at 15.0 US cents/kWh, second only to Singapore (18.1 cents)

Melbourne among the fastest-growing data centre hubs in the entire region (1,577% capacity growth since 2020)

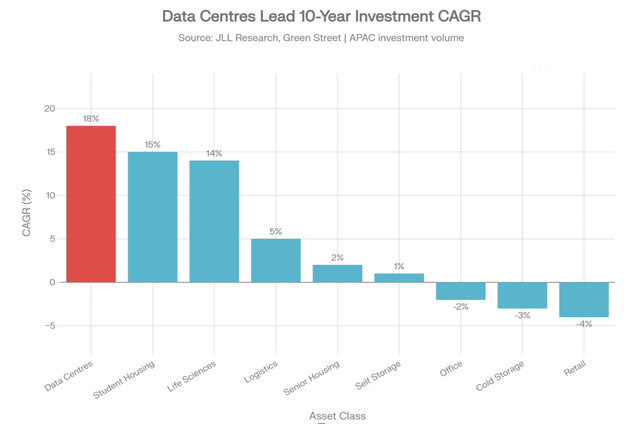

Data centres recorded the highest 10-year investment CAGR (18%) of any property type globally

JLL's year-end 2025 Asia Pacific Data Centre Report documents a regional buildout driven primarily by hyperscale commitments, with absorption, pre-leasing and capital deployment all reaching new highs Record colocation absorption hit 963 MW in H2 2025, driven by AI and cloud demand. Vacancy across Asia Pacific fell to 7% and is forecast to remain in the 6.5 to 7.0% range over the next few years, with 78% of the 4.8 GW pipeline expected by 2027 already preleased.

The capital required is staggering. JLL estimates that adding 24 GW of capacity between 2025 and 2030 will require US$772 billion under a high growth scenario, split between US$286 billion in real estate value creation and up to US$486 billion in GPU and networking fit-out. Colocation operators are expected to deliver up to 22 GW of that total, with hyperscale self-build accounting for a further 6 GW.

Data centres now hold the highest investment growth of any property type over the past decade, recording an 18% CAGR in annual investment volume (2016-2025), outpacing student housing (15%), life sciences (14%) and logistics (5%).

APAC data centre market at a glance (H2 2025)

Metric | Figure | Source |

H2 2025 absorption | 963 MW (record) | JLL Research |

Colocation vacancy (2025) | 7% (down from 20% in 2020) | JLL Research |

Pipeline to 2027 | 4.8 GW (78% preleased) | JLL Research |

Capacity CAGR 2020-2025 | 17% | JLL Research |

Forecast CAGR to 2030 | 19% | JLL Research |

2025 investment volume | US$15 billion | JLL Research |

Capital required 2025-2030 | US$772 billion (high growth) | JLL Research |

Enterprise rent growth (y-o-y) | +3% | JLL Research |

Hyperscale rent growth (y-o-y) | +2% | JLL Research |

Where Australia sits in this picture

Australia is not a bystander in this cycle. JLL's data places Sydney and Melbourne among the region's mature and high-growth markets respectively. Sydney recorded steady 10 to 25% CAGR growth in capacity over the past five years, while Melbourne's colocation market grew 1,577% since 2020, making it one of the fastest-growing hubs in all of APAC. In our recent analysis, we ranked Australia's top APAC data centres, with AirTrunk leading the pack.

However, Australia's position comes with structural challenges. Sydney's colocation electricity rate of 15.0 US cents/kWh is the second most expensive in the region, behind only Singapore at 18.1 cents. Grid connection delays in core markets now stretch beyond eight years, compared with 24 months in emerging markets. The Australian Energy Market Commission published draft rules in March 2026 proposing new technical standards for large data centres connecting to the National Electricity Market.

As we covered in our analysis of the NSW data centre consultation paper, the state government is laying out five principles that will shape the next decade of facility investment. Meanwhile, NSW attracted $136 billion in investment proposals through its Investment Delivery Authority and approved the Southern Hemisphere's largest data centre in just 12 months.

AirTrunk founder Robin Khuda has argued that Australia has a 12-to-18-month window to capture its share of the AI infrastructure boom. The JLL data reinforces that urgency.

Australian electricity cost in APAC context

Market | Electricity rate (US c/kWh) | Relative to Sydney |

Chennai | 8.4 | 44% cheaper |

Melbourne | 8.9 | 41% cheaper |

Tokyo | 14.3 | 5% cheaper |

Sydney | 15.0 | Baseline |

Singapore | 18.1 | 21% more expensive |

APAC vacancy is structural, not cyclical

The vacancy decline from 20% in 2020 to 7% in 2025 is not a temporary squeeze. JLL attributes it to hyperscale pre-commitments absorbing supply years before delivery, with 78% of the 4.8 GW pipeline to 2027 already locked in. This makes the remaining available capacity increasingly scarce and positions certified, power-secure facilities at a premium.

Regulation-led supply constraints in Singapore have resulted in demand spilling over to mature markets including Japan and Australia. The SIJORI (Singapore-Johor-Riau) growth triangle pact has driven major growth in Johor Bahru, which saw 5,262% capacity growth since 2020, the highest in the region. Hyperscalers are simultaneously establishing footprints in Thailand, India and the Philippines.

AI demand is reshaping absorption patterns

The JLL report confirms that AI workloads are the primary driver behind record absorption levels. Pre-commitments are being signed in emerging locations that provide scalability, assured power supply and market-friendly regulations, while core markets see AI demand spilling over as Singapore capacity remains constrained.

CBRE's Ada Choi flagged in mid-2025 that "developed markets like Japan, Australia and Korea will see heightened demand, with Singapore also attracting attention despite its supply limitations". Cushman and Wakefield's own H2 2025 report noted that APAC's pipeline expanded by 2,751 MW in the half to reach 19,371 MW, confirming the structural nature of this buildout.

Enterprise lease rents rose 3% annually due to limited supply in core markets, with demand for resilient, high-density facilities in prime locations driving pricing higher. Average hyperscale rents rose more modestly at 2% year-on-year as long-term pre-commitments absorbed supply before it reached market.

APAC colocation asking rents (2025)

Deployment size | Asking rent (US$/kW/mo) |

Less than 250 kW (all-in) | $403 |

250 kW to 1 MW | $239 |

1 to 5 MW | $151 |

5 to 20 MW | $137 |

More than 20 MW | $111 |

The neo cloud factor

One of the less-discussed dynamics accelerating demand in Australia is the rise of neo cloud providers. The 2025 Neo Cloud Study found that 84% of organisations in Australia and New Zealand currently use or intend to use GPU-as-a-Service by 2027, with enterprise compute demand growing at a 17% CAGR.

Unlike hyperscalers offering broad service portfolios, neo cloud operators deploy tightly integrated GPU clusters with high-bandwidth memory, low-latency networking and efficient cooling systems optimised specifically for AI workloads. Shane Hill, Chief Analyst at Integral Advice, noted that "using traditional or public cloud infrastructures for model training incurs exponential power, cooling and water costs" and that neo cloud providers "can counteract these issues and help executives reign in spiralling AI costs".

Venture Insights' 2026 Australia Data Centre Outlook highlights that neo cloud tenants are absorbing blocks of 10 MW to 50 MW, far exceeding traditional enterprise requirements of 1 to 5 MW. NEXTDC has positioned its sovereign facilities as a neo cloud hosting platform, with its Perth campus emerging as a potential gateway for neo cloud providers serving both Australian and Asian markets.

As we covered in our analysis of Macquarie Technology's $200 million NRFC deal, the company partnered with Dell Technologies to host a sovereign, NVIDIA-powered AI Factory within its new 47 MW IC3 Super West facility, due mid-2026, supporting private AI and neo cloud deployments.

The SUBCO SMAP hypercable, on track for full commissioning by May 2026, is also directly relevant. Bevan Slattery confirmed that 10 of 16 fibre pairs are already sold, with hyperscalers, carriers and neocloud providers leading demand. That connectivity backbone between Perth, Adelaide, Melbourne and Sydney underpins the low-latency, high-capacity requirements neo cloud tenants demand.

The investment cycle is shifting

JLL notes that data centre investment cycles in APAC are evolving toward recapitalisations and PropCo joint ventures, as most major fund managers have already partnered with regional operators. The US$15 billion in APAC investment volume in 2025, while down from the previous year's peak, demonstrates the sector's resilience.

Entity-level deals continue to dominate, reflecting the institutional maturity of the asset class. The projected 24 GW supply addition over the next five years is expected to open significant opportunities for development-stage investments in both equity and debt. As we explored at the Data Centre Leaders Summit in March, capital deployment, clean energy and building at scale are the sector's top priorities.

Vertiv and SUSE have warned that AI-ready data centres risk hitting an "energy wall" as Australia's hyperscale expansion strains power and cooling systems, with rising rack densities and specialised AI chips demanding fundamentally different approaches to facility design. For Australian operators, the ability to demonstrate certified, AI-ready capacity with secured power will increasingly determine capital allocation outcomes.

APAC capacity growth since 2020: top markets

Market | Growth since 2020 | Category |

Johor Bahru | 5,262% | Emerging hub |

Melbourne | 1,577% | High-growth mature |

Chennai | More than doubled | High-growth emerging |

Mumbai | More than doubled | High-growth emerging |

Seoul Capital Area | More than doubled | High-growth mature |

Sydney | 10-25% CAGR | Steady mature |

Tokyo | +626 MW (largest absolute addition) | Steady mature |

Singapore | 10-25% CAGR (supply-constrained) | Steady mature |

Why this is significant

Record absorption of 963 MW in H2 2025 confirms that AI demand is not speculative. Pre-leasing rates of 78% indicate hyperscalers are committing capital years ahead of delivery, creating a structural supply deficit across APAC.

Australia's high electricity costs and grid delays are strategic constraints, not just operational ones. Sydney's position as the second most expensive APAC market for colocation power means operators must differentiate on facility certification, power resilience and connectivity sovereignty.

Neo cloud absorption is a demand accelerant that most market commentary overlooks. With tenants taking 10 to 50 MW blocks and 84% of ANZ organisations planning GPU-as-a-Service adoption, neo cloud is rapidly becoming a primary driver of Australian data centre take-up alongside hyperscale.

The AEMC's draft grid connection rules signal that regulatory risk is now a core planning variable. Operators who fail to account for new grid performance standards may face delays that compound existing connection timelines.

US$772 billion in projected APAC capital investment (high growth scenario) creates unprecedented opportunity for certified, sovereign-grade Australian facilities positioned to capture both hyperscale pre-commitment and neo cloud demand.