At a glance

The Climate Council published Clouded Future: Managing the risks of the data centre boom on 3 June 2026, framing data centres as essential infrastructure and a “once-in-a-generation opportunity” to drive new clean-energy investment if growth is matched with renewables and firming.

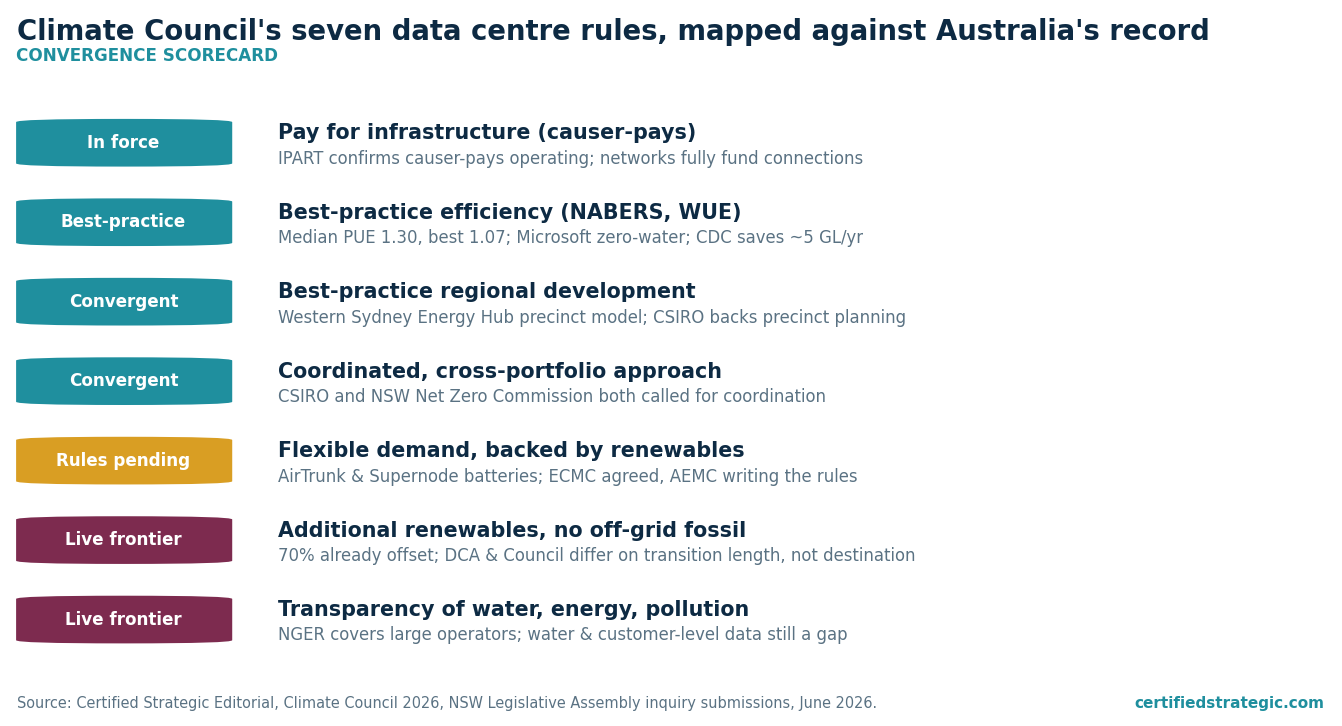

The report sets seven recommendations for governments, anchored on additional renewable energy, efficiency standards, flexible demand, causer-pays cost recovery, transparency, regional siting and coordinated planning.

Four of the seven are already in force or already best-practice in Australia: causer-pays connection charging, world-leading efficiency, precinct-based regional siting and cross-agency coordination.

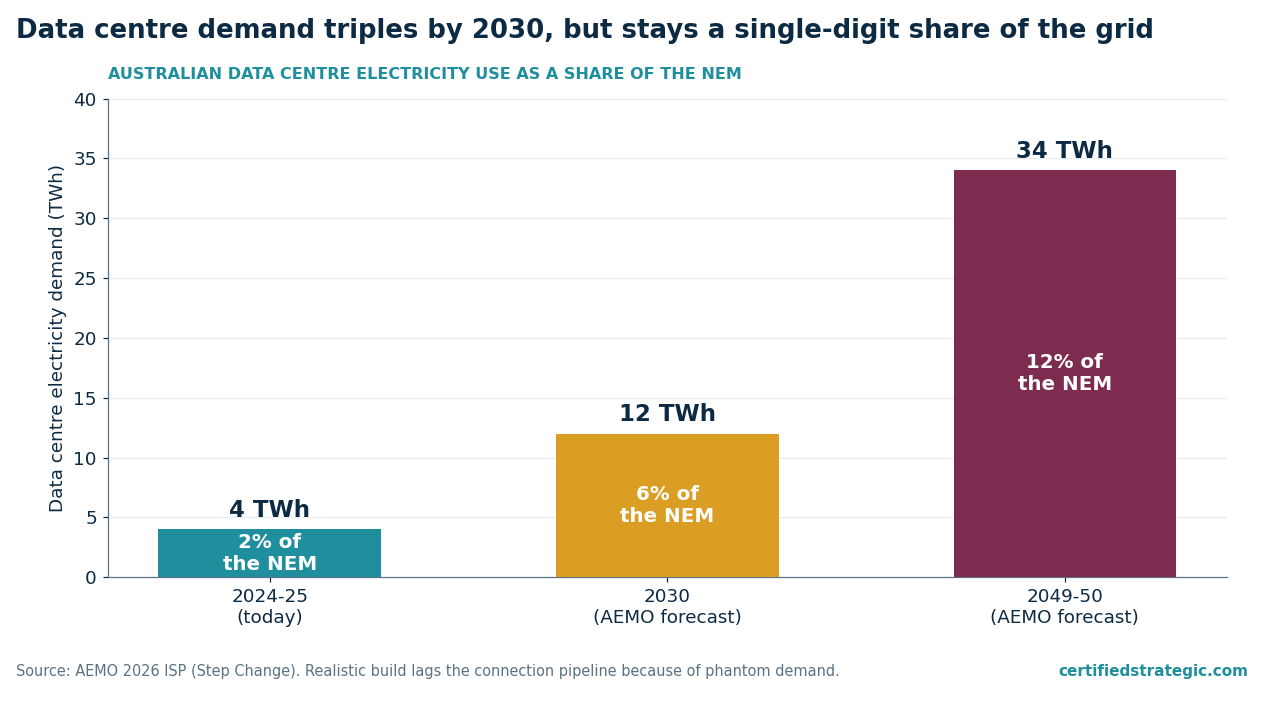

Data centres use about 4 TWh, or 2% of the National Electricity Market, today. AEMO expects that to triple to roughly 12 TWh, or 6% of the NEM, by 2030.

The two unfinished items are hard additionality for renewable contracts and national transparency on water and customer-level energy use. Both are where industry and the Council can move together.

The real binding constraint is the grid connection queue: Transgrid’s data centre enquiries top 14 GW with up to 70% speculative, while Neara estimates 10 GW of capacity already sits unused in NSW distribution networks.

The Council reframes the debate as a roadmap

The Climate Council has reset the terms of Australia’s data centre debate. Clouded Future, released on 3 June 2026 with a companion explainer, opens by describing data centres as the infrastructure behind hospitals, defence, transport and everyday digital life, then calls them a “once-in-a-generation opportunity” to underwrite new renewable generation. The Council’s position is conditional rather than oppositional: “With strong and enforceable policy, data centres can drive new clean energy investment and support a more resilient electricity system.”

As we documented in our analysis of all 119 NSW parliamentary inquiry submissions, the opposition that dominated the individual and templated submissions argued for pauses and hard caps. The Climate Council, an organisation that submitted to that inquiry, has instead published a roadmap for getting the buildout right. The disagreement that remains is about enforceability and pace rather than direction.

The numbers behind the report

The report sizes the load carefully. Data centres used around 4 TWh in 2024-25, about 2% of the NEM, equivalent to more than 700,000 homes. AEMO’s Step Change forecast has that tripling to nearly 12 TWh, or 6% of the NEM, by 2030, roughly enough to power every home in Victoria, and reaching 34 TWh, or about 12% of the grid, by 2049-50. We covered the same trajectory in our read of AGL’s 34 TWh demand forecast.

The headline risk numbers are conditional. If new data centre load is met with gas rather than renewables and storage, Baringa’s modelling for the CEFC projects wholesale prices up to 26% higher in NSW and 23% higher in Victoria by 2035, and a NEM up to 14% more polluting than it would otherwise be. The report is explicit that these outcomes are avoidable: matching load with additional renewables “would almost entirely avoid dumping extra costs onto households.”

The report also carries the phantom-demand caveat the industry has pressed throughout the inquiry. NSW shows 44 data centres totalling 11.4 GW in the pipeline, yet the industry expects only 1.2 GW to actually come online in Sydney by 2030. Our interactive Sydney data centre map tracks that pipeline site by site, with operators and planning-approval status for each. That gap between connection requests and built capacity is the same dynamic AEMO’s adviser Oxford Economics quantified as six of every seven megawatts never materialising, which we set out in our coverage of AEMO’s 5.4 GW pipeline. The report leans on the gross pipeline to size the risk and on the net figure to caveat it. Both are accurate.

Where the industry already meets the brief

Read against the inquiry record and current operator behaviour, four of the seven recommendations describe practice that already exists in Australia, one is willing but waiting on rule changes, and two are the live frontier.

Climate Council recommendation | Status in Australia | What the record already shows |

Pay for energy and water infrastructure (causer-pays) | Mostly in force | IPART confirmed to the inquiry that a causer-pays framework already operates, and declined Sydney Water’s 250 ML/day forecast as too uncertain to price. NSW networks state connecting customers “fully fund their portion” with upfront contributions and guarantees. |

Best-practice energy and water efficiency | Already best-practice | Australian data centres run a median PUE of 1.30 and a best of 1.07, ahead of the global average. Microsoft moved new facilities to zero-water cooling, and CDC’s liquid cooling saves an estimated 5 GL a year. Government-contracted facilities have required five-star NABERS since 1 July 2025. |

Encourage best-practice regional development | Aligned | The Western Sydney Data Centre Energy Hub already proposes shared precinct infrastructure, and CSIRO and the NSW Net Zero Commission both recommended precinct-based planning to the inquiry. |

Coordinated, cross-portfolio approach | Aligned | CSIRO and the Net Zero Commission both called for coordination across planning, energy and water, the same machinery the report asks governments to build. |

Flexible demand, backed by renewables | Willing, rules pending | AirTrunk is building a battery beside its 320+ MW SYD3 site, and Supernode hosts one of the NEM’s largest batteries. Energy ministers agreed on demand flexibility on 8 May 2026 and tasked the AEMC with the rules. |

Additional renewables and firming, no off-grid fossil | The live frontier | Industry already offsets about 70% of its energy use through certificates and PPAs, and the Clean Energy Council told the inquiry operators are “actively seeking” renewable contracts. Additionality and a ban on off-grid gas are the unresolved questions. |

Transparency of water, energy and pollution | Genuine gap | Large operators report energy and emissions under NGER, but sub-threshold operators, customer-level use and water draw are largely undisclosed. |

Source: Certified Strategic Editorial, Climate Council 2026, NSW Legislative Assembly inquiry submissions, primary operator disclosures, June 2026.

On the efficiency and cost-recovery fronts in particular, the report is asking governments to standardise what leading operators already do. Microsoft’s zero-water cooling, CDC’s liquid-cooling savings and the sector’s PUE figures are the kind of evidence we tracked in which operators already meet the national expectations. The causer-pays mechanism the Council wants for shared infrastructure is the same one IPART confirmed is already operating in NSW, a point worth adding to the record because the report does not mention IPART by name.

The two items that are unfinished

Two recommendations describe real work that is not yet done, and both are areas where the industry can move toward the Council.

The first is additionality. The report’s sharpest argument is that a power purchase agreement is not the same as new capacity: “PPAs do not necessarily lead to new renewable generation or storage capacity being built. They are often contracts with capacity that was already planned or operational.” The Council wants pre-financial-close PPAs as the test, so that a data centre’s demand demonstrably underwrites a project that would not otherwise have been built. That is a defensible standard, and some operators already meet it. The Google and AirTrunk Mulwala solar PPA and Amazon’s 430 MW of battery-backed renewables show demand being matched to new generation and storage. The report’s concern is making that the floor, and pairing it with a prohibition on off-grid gas of the kind proposed at Southern Highlands.

The industry’s answer to that standard is about timing. Responding to a near-identical set of public-interest principles in March 2026, Data Centres Australia chief executive Belinda Dennett said the sector is already a major investor in renewables through power purchase agreements and large-scale generation certificates, and argued that matching load from day one does not reflect renewable build timelines. “The bottleneck is not off-take, it is grid connection and approvals,” Dennett wrote, backing a phased approach aligned with renewable delivery timelines and applied consistently across all large energy users. The Climate Council’s own recommendation allows a transition of up to three years to reach 100% renewable procurement, which sits close to that position. The two sides differ mainly on the length of the transition while agreeing on the destination.

The second is transparency. Better disclosure costs operators little and answers the water questions that drove much of the inquiry opposition. Water draw is largely undisclosed at the facility level, customer energy use sits outside operator reporting, and smaller facilities fall below the NGER threshold. A nationally consistent reporting standard for water, energy and emissions would replace the contested estimates that filled the inquiry with metered fact. For an industry whose numbers are routinely misread, that disclosure is a defensive asset worth volunteering.

The grid is the gate

The constraint that decides Australia’s data centre future is the connection queue rather than the power behind it. Transgrid has fielded data centre connection enquiries for more than 14 GW, close to the entire NSW peak winter load, and Neara estimates as much as 70% of that is speculative. NSW’s own Investment Delivery Authority made the same point in hard numbers in March 2026, endorsing 15 data centre projects worth A$51.9 billion while setting aside around A$40.7 billion of proposals as premature or overly speculative. This is the phantom-demand dynamic AEMO’s adviser Oxford Economics quantified as six of every seven requested megawatts never materialising, the gap between connection requests and built capacity we tracked in our coverage of AEMO’s pipeline.

Neara, the Sydney-founded grid-modelling company now valued at AU$1.1 billion, argues the slack to absorb real demand already exists. Its physics-based digital twins estimate up to 10 GW of latent capacity in NSW distribution networks, more than the entire Central-West Orana renewable energy zone. Neara’s commercial lead Tom Gooch frames the problem as visibility rather than scarcity: developers cannot see the network’s granular capacity picture, networks cannot see which applications are real, and communities cannot see what their local grid could host. Each participant reads the same problem from a different seat, using data no other participant can see. Our interactive Melbourne data centre map is a working example of the shared picture this requires, overlaying the facility pipeline against grid capacity and substations in one view.

Unlocking distribution-level capacity does not on its own connect a gigawatt hyperscale campus, which plugs in at transmission level, and it does not settle the separate questions of generation mix or water. What it does is compress the part of the process everyone agrees is broken: siting and connection. Overseas networks already use the approach to hand developers pre-screened shortlists of viable, grid-and-environment-friendly sites, so networks receive fewer and higher-quality applications and can deploy capital with confidence. Data centre developments can also fund upgrades to ageing local infrastructure, improving reliability for the communities that host them.

This is why the grid question reinforces the convergence story. The fix needs no new legislation and asks mainly that networks and developers share what they each already know. It speeds the renewable and data centre connections the Climate Council wants delivered at pace, it relieves the connection-and-approvals bottleneck Data Centres Australia named as the binding constraint, and by unlocking existing capacity it avoids augmentation costs that would otherwise land on households.

What this means

The Climate Council has handed the industry a constructive document and a clear set of expectations, most of which the better operators already satisfy. The Australian government’s national expectations for data centres and the NSW consultation paper’s five principles already point the same way, as do the renewable commitments in the Anthropic Australia MoU. Three things are worth holding in view.

First, the report shifts the burden of proof. The question is no longer whether data centres should be built, but whether each project can show additional renewables, efficiency and disclosure. Operators that can document those today gain a planning and reputational edge.

Second, additionality is the gating item for approvals. The pipeline numbers will keep moving with phantom demand, but the standard that decides projects will be whether each one underwrites new generation.

Third, the connection queue is the gate worth unclogging. Transparency and physics-based network modelling are the fastest available wins for both sides, because they speed clean connections without legislation or trade-off. The watch items are the AEMC’s demand-flexibility rules, the AER’s connection-charge review, whether networks adopt upstream capacity-sharing with developers, and whether NSW and the Commonwealth convert the federal expectations into the enforceable, nationally uniform standards the Council is asking for.