At a glance

A Guardian report on 1 July drew together Reserve Bank inflation concerns, a Transport for NSW submission on freight operators leaving Sydney, and a tri-state moratorium campaign into one warning that data centres are crowding out land and housing.

CBRE’s 1H26 industrial and logistics report puts national vacancy at 3.2%, unchanged and below its own 3.4% forecast, with net absorption above 1.4 million sqm, more than double the second half of 2025.

Transport for NSW told the state inquiry that land scarcity is pushing major freight operators out of Sydney toward Brisbane and Melbourne, a concern the logistics sector says is real and specific.

Roughly 44GW of data centre connection requests sit against about 6GW the central grid scenario expects to be built, so much of the land said to be “snapped up” is attached to applications that will not energise.

NEXTDC’s A$8.2 billion senior debt platform, underwritten by a domestic and international banking syndicate, sits behind contracted load, which shows where planning approvals could be weighted toward projects that will actually build.

What the week’s coverage assembled

Four separate items landed within days of each other and were read as one indictment of the data centre boom. The Reserve Bank’s June board minutes, reported by the Guardian, noted that stronger than expected business investment, much of it data centre capex, could add to inflation. The Australian Bureau of Statistics reported that commercial and industrial building approval values hit a record high in May on new data centre projects, after naming data centre equipment as the driver of the March quarter capex surge. Transport for NSW warned the state parliament inquiry that industrial land is under pressure. And CBRE published its half-year vacancy read.

Land, power and water have been the story for a year. Westpac senior economist Pat Bustamante said that if data centre spending competes for land and resources, the Reserve Bank would lift rates to make room, and home building would feel it first. That rates-and-mortgages framing is why Labor backbencher Ed Husic called for governments to “pump the brakes,” and why an alliance of community groups in New South Wales, Victoria and Western Australia is calling for a halt to new approvals. The concern deserves a serious answer rather than a dismissal.

CBRE’s own numbers describe a stable market

The report doing much of the work in the coverage does not show data centre demand absorbing industrial land fast enough to crowd logistics and housing off it.CBRE puts national industrial and logistics vacancy at 3.2% in the first half of 2026, unchanged on the prior half and below its own earlier forecast of 3.4%. Net absorption ran above 1.4 million sqm, more than double the second half of 2025, which CBRE reads as the market absorbing new supply faster than expected. Perth tightened to 1.0%, Melbourne held at 4.7%, and the largest single move was Sydney rising to 3.5%, concentrated in older stock in the Outer South West rather than in modern facilities.

CBRE’s own forward view is that vacancy peaks around 3.5% in the second half of 2026, stays below the sector’s 4% equilibrium mark, then trends lower from 2027. Its structural worry is the shortage of serviced and appropriately zoned industrial land, a constraint it ties to population growth, e-commerce and supply chains, and one that would exist without a single data centre. The report does not mention data centres; the link to the AI buildout was drawn by the surrounding coverage.

The freight sector’s concern is real and geographically specific

Taking the numbers seriously does not mean waving away the logistics case, which is narrower and more concrete than the inflation framing. Transport for NSW told the inquiry that land scarcity is “causing major freight and logistics operators to leave Sydney,” relocating to Brisbane or Melbourne where suitable land is cheaper, even as it acknowledged vacancy has improved. The Australasian Supply Chain and Logistics Association put the structural point plainly through chief executive Steven Ballerini: a distribution centre has to sit close to the population it serves, so it cannot move to the urban fringe without adding cost, distance and emissions.

That is a genuine competition for a specific type of parcel, transport-connected land near markets. The Lane Cove Responsible Planning Group’s figure, that five planned data centres would take about 40% of one suburb’s industrial land, is the local version of the same worry. The question is not whether the competition exists. It is how much of the demand pressing on that land is real.

How much of the land demand is speculative

A large share of it is not yet real, and that changes the policy calculus. Network providers passed roughly 44GW of data centre connection requests to AEMO for its 2025 planning inputs, against the roughly 6GW the central scenario expects to be built, a gap examined in our analysis of phantom demand in the connection queue. Cushman & Wakefield reached the same conclusion from the capital side, naming Australia among markets “increasingly concerned with speculative demand and low project realisation rates,” where grid applications are “used strategically by landowners and developers to inflate land values.” We set that out in our coverage of Australian data centre land at an APAC premium.

A lodged connection request is not itself a land parcel, but Cushman’s point is that land positions are taken and priced off exactly these grid applications. If much of the land supposedly removed from housing and logistics is attached to applications that will never connect, a blanket moratorium freezes the projects that are real while leaving the speculative land positions untouched. The formal transmission connection queue, now 5.4GW across eleven projects split close to 60% New South Wales and 40% Victoria, is a fraction of the requests lodged, and it is a public instrument for telling a genuinely executable project from a parked land position.

The distinction is one the operators are pressing themselves. At the Committee for Economic Development of Australia’s State of the Nation conference in late June, CDC Data Centres chief strategy officer Jack Dan warned that rapid growth “attracts a significant amount of speculators” and “fly-by-night, cowboy-type behaviour,” describing landowners who “see a power line in the background” and lodge proposals that clog planning, water and utility pipelines without the capital, underwriting or customers to build, as InDaily reported. His fix is applicant vetting: screening the proponent behind an application before it consumes a queue slot.

Capital already sorts real projects from speculative ones

Where a project carries secured power, a connection agreement and a contracted customer, the capital tends to follow. NEXTDC holds roughly A$8.4 billion in pro forma liquidity, including an A$8.2 billion senior debt platform lifted by an A$1.8 billion close with a domestic and international banking syndicate on 5 May 2026, as we set out in NEXTDC’s four-city Asia pipeline analysis. Behind that capital sits contracted demand: pro forma contracted utilisation rose 250MW in a single quarter to 667MW, and the forward order book grew 83% to 544MW. On our reading, senior debt at that scale tracks contracted load rather than lodged applications, which makes a project’s capital structure a useful signal of whether it is real. NEXTDC chief executive Craig Scroggie framed the raise the same way, saying “capital is selective” and “is backing contracted, deliverable capacity with a clear path to energisation and revenue.”

The land backed by bankable, contracted, capital-committed load is the land that should clear planning quickly, while the speculative overhang is the part worth slowing.

A coordination path, weighted to contracted power

Data Centres Australia has been making this case inside the same coverage. Chief executive Belinda Dennett, citing the CBRE figures, said the answer is “to release and service more land and plan it well, putting the right uses on the right land,” so freight keeps the transport-connected sites it depends on while data centres deliver investment and infrastructure. She agreed Sydney needs a coordinated approach but disputed that it is a contest between the two sectors, and called a moratorium the wrong tool.

Weighting approvals toward projects with contracted power and a named customer addresses the freight sector’s specific concern while keeping executable projects moving. It is the same lever running through the current rule-writing: how the Senate inquiry treats applicant vetting, and how the Australian Energy Market Commission’s new access standards for large loads are drawn. Across the signals we monitor on our proprietary dashboard, which tracks submissions, operator commentary, connection data and community campaigns in near real time, applicant vetting is the point operators, regulators and community advocates are separately converging on. We set out where each government sits on this in our review of Australian data centre policy by state, and the broader question of consent in data centres and social licence.

What to watch

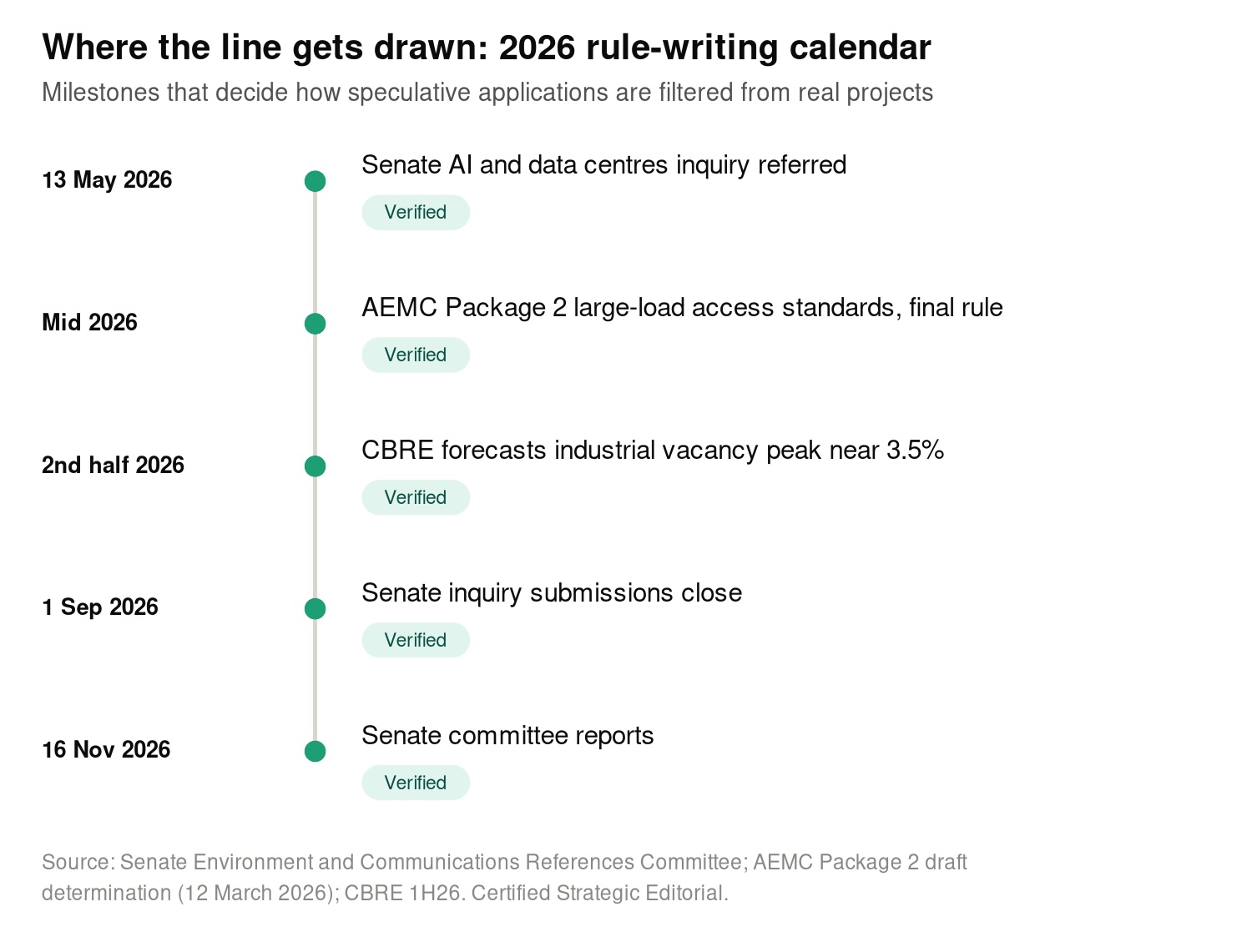

The Senate inquiry into data centres and AI is taking submissions until 1 September 2026 and reports by 16 November 2026, and whether it lands on applicant vetting and upfront conditions will decide if new rules clear the queue or simply narrow it. The Australian Energy Market Commission expects to finalise its Package 2 large-load access standards, lifting the threshold to 30MW, by mid-2026, and AEMO’s next queue update will show how much speculative demand has dropped away. On the macro side, the Reserve Bank’s rate path through the second half of 2026 will test the inflation framing, and CBRE’s next half-year read will show whether Sydney’s Outer South West vacancy holds or tightens. Each one moves the line between a real project and a parked one.