At a glance

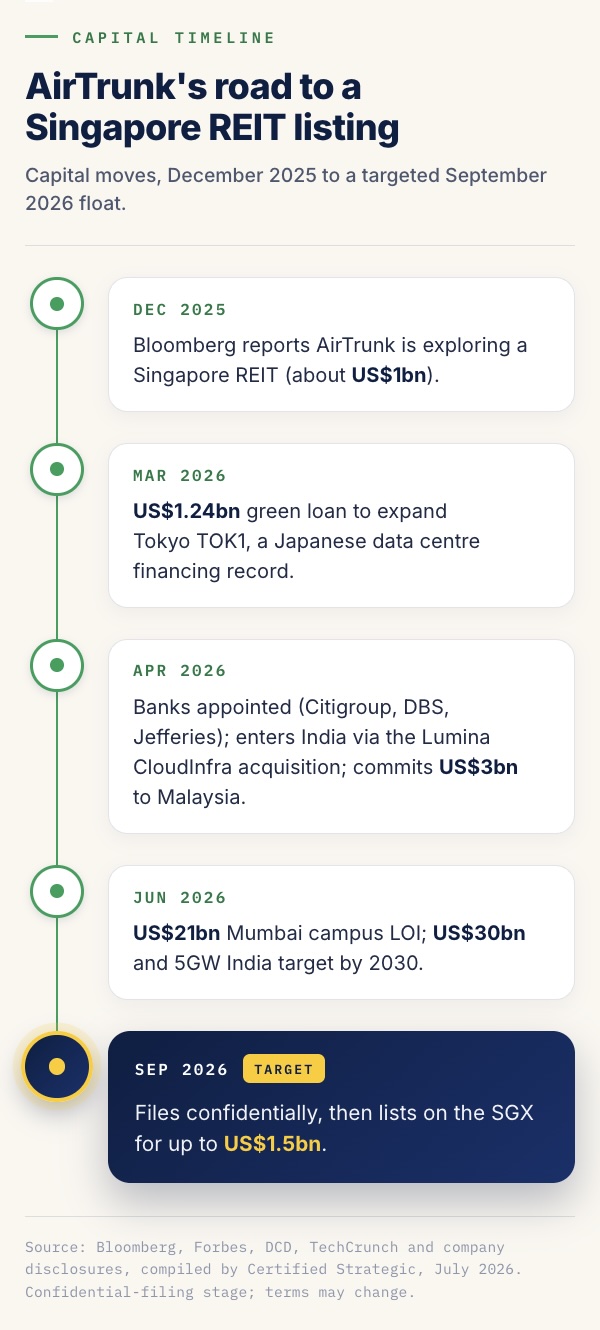

AirTrunk is reported to be about to file confidentially for a Singapore REIT initial public offering, as soon as this week, targeting a September 2026 listing and a raise of up to US$1.5 billion.

At the reported size the float would rank as Singapore’s largest IPO since 2017 and, if it prices there, the largest data centre REIT listing the exchange has done, ahead of NTT DC REIT’s US$773 million debut in July 2025.

The listing is a capital-recycling move by owners Blackstone and the Canada Pension Plan Investment Board, under two years after their A$24 billion (more than US$16 billion) acquisition, rather than a sale of the platform.

A REIT lists on stabilised, contracted, income-producing assets, which places AirTrunk at the bankable end of the market and separates it from the speculative grid-queue activity now under scrutiny in Australia.

The float eases AirTrunk’s cost of capital, yet the binding constraint on its Australian growth is grid power and planning consent.

AirTrunk nears a confidential filing in Singapore

AirTrunk is about to file confidentially for an initial public offering of a real estate investment trust in Singapore, as soon as this week, according to Bloomberg reporting carried by w.media. The Sydney-founded platform is targeting a September 2026 listing and is working with Citigroup, DBS Group and Jefferies on the deal. AirTrunk declined to comment.

The number has moved. When Bloomberg first reported the plan in late December 2025, the raise was framed at about US$1 billion. By April 2026, when the banks were appointed, reporting had lifted it toward US$1.5 billion. At that level it would be the largest IPO in Singapore since NetLink NBN Trust raised US$1.7 billion in 2017, and at the reported size roughly double NTT DC REIT’s US$773 million debut in July 2025, the largest data centre REIT listing the exchange has done. Negotiations continue and the terms may still change.

A capital-recycling float by Blackstone and CPPIB

Blackstone and the Canada Pension Plan Investment Board completed their acquisition of AirTrunk in September 2024 at more than US$16 billion (A$24 billion), the largest data centre transaction in Asia-Pacific history, as we set out in our coverage of AirTrunk’s two entries in the 2026 data centre M&A top 10. Under two years on, that is far too early to sell a platform still being built out at this pace.

A REIT is a recycling vehicle. The owners drop stabilised, income-producing assets into a listed trust that yield investors will pay a premium to hold, pull cash back out, and keep the private development platform and its growth pipeline. The listed trust then becomes a permanent-capital home for mature assets and, over time, a buyer of stabilised campuses from the development arm. Blackstone has run versions of this playbook across logistics and digital infrastructure before. For AirTrunk it opens a cheaper, repeatable funding channel just as the platform commits tens of billions across the region.

Singapore holds the REIT capital and the template

Singapore has what the ASX lacks for a trust like this. It runs a deep REIT market, with trusts making up about a tenth of the exchange’s market capitalisation, and it already has a specialist data centre REIT template in the pure-play Keppel DC REIT and Digital Core REIT, the recently listed NTT DC REIT, and diversified holders with heavy data centre exposure such as Mapletree Industrial Trust. It offers a US-dollar listing convention suited to a pan-Asian income stream and a pool of sovereign and institutional cornerstone capital. GIC anchored the NTT deal a year ago.

The ASX offers a thinner pool of infrastructure-income buyers, and AirTrunk’s portfolio is pan-APAC rather than Australia-weighted, which makes a neutral regional hub the logical venue. Australia originated the company; Singapore captures the listing, the fee pool and index inclusion.

How the REIT fits AirTrunk’s 2026 capital programme

The float only makes sense against how much capital AirTrunk has committed this year. A REIT is the release valve that funds a pipeline of this size without Blackstone and CPPIB writing ever-larger equity cheques.

The pattern is a platform funding an offshore build-out while opening a public channel to recycle capital out of its stabilised assets. The US$30 billion India commitment alone dwarfs anything AirTrunk has announced at home this year.

Only contracted income can carry a REIT

Institutional cornerstones and REIT managers underwrite the certainty of the income, which means stabilised assets, creditworthy hyperscale tenants and long weighted-average lease expiries. The fact that AirTrunk’s owners can assemble a floatable income trust at all places the platform at the contracted, bankable end of the market. This is the same distinction the Australian sector is now drawing in public between real projects and speculative ones, a debate we examined from the grid side in Australia’s data centre gold rush has a ghost town problem and from the capital side when Cushman put Australian data centre land at an APAC premium. AirTrunk sits on the executable side of that line.

A public listing also brings public reporting. Listed S-REITs report portfolio occupancy, lease expiry profiles, tenant concentration and contracted capacity every period, the kind of standardised, audited detail that private platforms are not required to publish. If AirTrunk's Australian campuses sit in the trust, that reporting would give the market a clearer, verifiable read on contracted hyperscale income here. Which assets go into the REIT has not been reported, and that composition is the detail still to be confirmed.

What a public benchmark means for Australian valuations

If Singapore prices a pan-APAC hyperscale REIT this year, it creates a live public comparable for contracted data centre income. That reference point flows back into how the market values Australian operators, from NEXTDC and CDC Data Centres to the neocloud cohort signing multi-megawatt leases across Sydney, Melbourne and Perth. A visible yield for stabilised hyperscale income is more useful to that market than the private-transaction guesswork it relies on now.

The counterweight is where AirTrunk’s own capital is landing. Its founding market remains substantial, with more than 1.2GW of operating and committed capacity across five Sydney and Melbourne campuses and MEL2 adding A$5 billion of investment. Yet the platform’s largest new commitments now sit in India, Japan and Malaysia, and AirTrunk operates past 3GW of operating and planned capacity across 20 campuses in six markets. Australia has become one node in a regional portfolio, no longer the platform’s centre of gravity. Consistent with the US$772 billion APAC supercycle JLL has mapped, the addressable market has gone regional while Australia’s own pipeline keeps growing. The open question for policymakers is what would keep more of that capital landing here.

The constraint in Australia is power

The REIT gives AirTrunk cheaper and deeper capital. Capital is not the scarce input in the Australian build. Power and social licence are. AirTrunk’s separate proposed campus at Kemps Creek in Sydney’s west, its SYD4 site, is sized at 1.2GW and would be the first Australian data centre to pass a gigawatt. The grid to serve it is being purpose-built, with Endeavour Energy and Transgrid constructing a new bulk supply point at Kemps Creek to meet Western Sydney demand. The project has also drawn objections from Penrith City Council and nearby schools, and the NSW Environmental Protection Authority found the project’s environmental impact statement did not provide the information needed to complete its assessment of air quality and noise. A larger balance sheet does not shorten a grid build or resolve a planning objection, a dynamic we traced in where data centre regulation ends and engagement begins and in AEMO’s 2026 Integrated System Plan, which names data centres as a major new driver of electricity demand. Financial engineering in Singapore is the straightforward half of the equation. Energising a gigawatt in Western Sydney is the hard half, and it is the gating item on domestic growth.

AirTrunk’s offshore markets offer both capital and megawatts more readily than Australia, which is why so much of the platform’s new spend is landing in Mumbai, Johor and Osaka rather than at home. For readers new to why these facilities are power-bound, our explainer on what an AI data centre is sets out how the current build differs from the generation before it.

What to watch

Most of what matters is still unfiled. The prospectus will set the final raise, name the cornerstone investors, and show the yield Singapore puts on contracted hyperscale income. The number to watch is the asset list. Which AirTrunk campuses go into the trust decides how much of this is an Australian story, and whether local infrastructure ends up inside a Singapore-listed, Singapore-governed vehicle. A September listing would put a public price on income the platform has so far kept private.