At a glance

As of late June 2026, Anthropic’s process to buy 300 to 500MW of Australian capacity to train its models is still live and unsigned, with CDC Data Centres reported as front-runner ahead of AirTrunk, NEXTDC and Firmus Technologies (AFR Street Talk).

A CDC win would sit on top of the separate 555MW US contract CDC signed in May, which AFR confirms is not Anthropic, taking CDC’s contracted book beyond 1GW across FY28 and FY29.

Power and grid connection, more than brand, decide this contest: Wood Mackenzie told CNBC on 25 June 2026 that securing power is now a harder constraint than land, financing or permits, and AEMO forecasts data centre load reaching 12.0TWh by 2030 against more than 10GW of New South Wales connection requests.

The hunt tracks Anthropic’s growth: the company raised US$65 billion in May 2026 at a US$965 billion valuation, with revenue run-rate past US$47 billion, and is staffing six Sydney data centre roles to source and run local capacity (CNBC, 25 June 2026).

Anthropic’s Australian push runs through its 31 March 2026 National AI Plan MoU and two early Australian government customers, the Fair Work Commission and the Australian Signals Directorate, aligning with CDC’s government and Defence-grade profile.

The contract is still live as of late June 2026

On 25 June 2026, CNBC reported that Anthropic is racing to add AI data centre capacity across the Asia Pacific, with six of its open data centre roles based in Australia. The Australian contract at the centre of that push, 300 to 500MW to train its models, remains unsigned as of late June, which keeps the question of who wins it live.

The AFR Street Talk column of 27 May 2026 reported that Anthropic has been running a process to select an Australia-based data centre provider, with the aim of buying 300 to 500MW of computing capacity to train its large language models locally. The column named four parties that have pitched: AirTrunk, NEXTDC, Infratil’s CDC Data Centres, and Oliver Curtis and Tim Rosenfield’s Firmus Technologies.

On the leaderboard, Street Talk reported that multiple sources placed CDC Data Centres as front-runner, to the point that Infratil investors had expected Anthropic to be named at the company’s 26 May investor day. No name was disclosed. As of that week Anthropic was still in conversations with several parties and had not signed a lease, so the contest remains open and CDC’s position is a reported lead rather than a concluded deal.

AFR stated plainly that Anthropic is not the unnamed client behind the 555MW contract CDC announced on 6 May 2026. That deal is with a separate US investment-grade customer. The significance for CDC is structural: winning Anthropic would mean delivering a second large block on top of the 555MW already contracted.

CDC’s government pedigree and campus headroom

CDC Data Centres carries the campus footprint and government-grade pedigree that map to the way Anthropic has entered Australia. The company’s Sydney pipeline includes the Marsden Park campus, approved in November 2025 at 504MW and scalable to 1GW, which is the kind of headroom a 300 to 500MW anchor tenant requires. Infratil, CDC’s majority owner, has the balance sheet and the capital-markets access to fund accelerated construction against a signed anchor.

There is an alignment argument as well. Anthropic’s Australian entry has run through Canberra: the National AI Plan MoU signed with the Albanese government, and two early Australian government customers in the Fair Work Commission and the Australian Signals Directorate. CDC holds Hosting Certification Framework Strategic-tier accreditation and built its business on Australian government and Defence workloads. For a buyer whose Australian foothold is government-relationship-led, the government-grade operator is the natural counterpart.

A CDC win would add a second US mega-contract

A CDC win would turn on capacity and grid more than commercial appetite. The 555MW deal signed in May is scheduled to deliver across FY28 and FY29. A 300 to 500MW Anthropic contract layered on the same development window would push CDC’s contracted position well beyond 1GW and concentrate a large share of its near-term pipeline into two US AI tenants delivering at once. Whether that is executable comes down to firmed grid connection and construction sequencing across the Marsden Park and broader Sydney footprint.

That filter applies to every bidder. AEMO’s July 2025 data centre demand report put the category at 3.9TWh in the 2025 financial year and forecast growth to 12.0TWh by 2030, near 6% of the National Electricity Market. AEMO logged 44GW of data centre connection requests against roughly 6GW of prospective capacity its central scenario requires. New South Wales has logged more than 10GW of connection requests over 18 months, more than half the state’s peak demand, per submissions to its parliamentary inquiry. Whichever operator can firm power for a 300 to 500MW block on Anthropic’s timeline holds the deciding card, which is why both sides of the table are now staffing power-procurement specialists. Wood Mackenzie’s APAC power and renewables analyst Xiaonan Feng framed the regional constraint to CNBC on 25 June 2026: “securing power is becoming more challenging than securing land, financing or permits.”

The rest of the field

Three other operators were in the process, each with a different strength. The full field of Australian data centre operators sits in our directory.

Operator | Position for a 300 to 500MW anchor | Recent signal |

CDC Data Centres | Government-grade, Marsden Park 504MW scalable to 1GW, Infratil-funded | Reported front-runner per AFR; separate 555MW US deal signed 6 May 2026 |

AirTrunk | 1.2GW SYD4 campus at Kemps Creek, the largest yet proposed in Australia, Blackstone-backed | Recruiting renewable and carbon procurement to source PPAs |

NEXTDC | ~550MW Western Sydney AI campus anchored by OpenAI; deep listed-operator pipeline | Anchored the largest disclosed AI-lab tenancy in the country |

Firmus Technologies | GPU-first neocloud scaling its 1.6GW Project Southgate alliance with CDC and NVIDIA; first 150MW stage under construction | ASX float pushed beyond September 2026; pitched for the Anthropic process |

Source: Primary company disclosures and NSW planning records, June 2026.

AirTrunk operates the highest-capacity proposed campus in the country and the capital depth to build at scale, which makes it the natural counter-bid on raw headroom. NEXTDC has already proven it can anchor a US frontier-AI tenant at this scale with OpenAI, and the question for a second mega-tenant is how much contemporaneous Western Sydney power it can commit. Firmus is the outsider at this capacity tier, and an Anthropic anchor would reshape both its build-out and the timing of its float, which gives it the sharpest incentive to bid hard on price.

Where the Australian deal sits in Anthropic’s global build

Anthropic’s capacity hunt has accelerated with its growth. The company raised US$65 billion in May 2026 at a US$965 billion valuation, with its revenue run-rate crossing US$47 billion that month, and has said its consumer growth is straining existing infrastructure (CNBC, 25 June 2026).

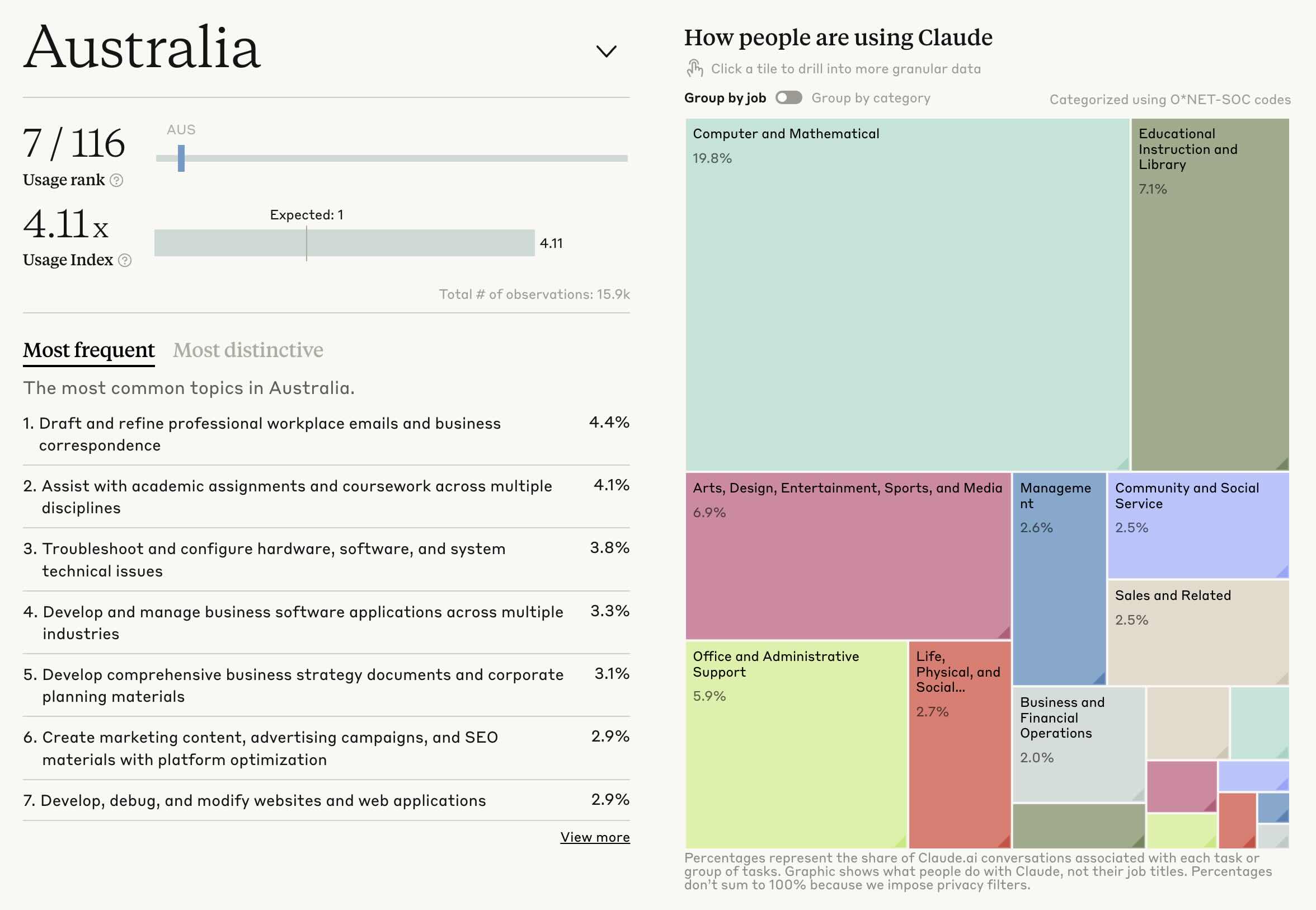

Australia is one of Claude’s strongest markets. On Anthropic’s Economic Index, the country ranks 7th of 116 for Claude usage and runs at 4.11 times the level its population would predict, off 15.9k observations. Computer and mathematical work is the single largest use at 19.8%, ahead of educational and creative tasks.

Anthropic Economic Index panel for Australia, showing a Claude usage rank of 7 out of 116 countries and a usage index of 4.11 times the population-expected level across 15.9k observations, with a treemap of how Australians use Claude led by computer and mathematical work at 19.8 percent, ahead of educational instruction at 7.1 percent and arts and design at 6.9 percent.

Anthropic Economic Index panel for Australia, showing a Claude usage rank of 7 out of 116 countries and a usage index of 4.11 times the population-expected level across 15.9k observations, with a treemap of how Australians use Claude led by computer and mathematical work at 19.8 percent, ahead of educational instruction at 7.1 percent and arts and design at 6.9 percent.

Australia ranks 7th of 116 countries on Anthropic’s Economic Index and uses Claude at 4.11 times its population-expected share. Source: Anthropic Economic Index, country usage, last updated 24 March 2026.

The Australian process clarifies a question that has run alongside it: why a company building its own data centres elsewhere would lease here. Anthropic’s US$50 billion Fluidstack programme, announced on 12 November 2025, is a custom self-build across Texas and New York, financially backed by Google. The Australian 300 to 500MW band, by contrast, is a capacity buy from a domestic provider. The split is deliberate. Anthropic self-builds at scale in the United States, where it has the programme size and a creditworthy backer, and leases internationally, where a local operator already holds the scarce power and planning approvals that a foreign entrant would spend years assembling.

Read against that programme, the Australian band is the second-largest single direct-facility commitment Anthropic has on the public record, behind only Lake Mariner at 360MW. It is also the company’s first non-US hyperscale-tier procurement, which is why the Sydney Compute hiring moved from operations roles into transaction and energy leadership over the second quarter.

What to watch next

Four signals will move first. The provider announcement is the obvious one, and on the cadence of OpenAI’s December 2025 NEXTDC naming it would be plausible across the second half of 2026. The structure of the winning bid is the second: a straight colocation lease would mirror the Fluidstack pattern, while an anchor-tenant build would align more directly with the National AI Plan expectations on energy additionality. Third is the energy commitment, since the selected campus will be read against the Department of Industry’s national expectations and the AEMC’s large-data-centre connection rule due mid-2026. Fourth is Firmus, whose float timing would tell the market whether it secured an anchor or remained a challenger.

For the operator audience, the capacity tier is set and the shortlist is named. For investors, a concluded Anthropic deal would add a second hyperscale-class commitment to the Australian book within a year of the OpenAI announcement. The market is absorbing frontier-AI demand on schedule.